Even in exuberant markets, there are mispriced stocks. Those who tell you otherwise aren’t bothering to look or going through the weeds. They’re staring at the same 300 tickers as everyone else and calling it “the market”.

The Shiller P/E passed 40x last month. The only other time it reached this level was during the dot-com bubble. (The data goes back to 1881.) But if you’re only fishing in one pond and conclude that valuations are universally unhinged, that’d say more about your fishing habits than the ocean itself.

The Shiller P/E captures just one geography and one narrative. Koyfin says there are >55k primary listed stocks out there across global markets. A tiny number of these are great, most are mediocre, but a surprising number are priced as if investors forgot to run the numbers. The dispersion of valuations has rarely been wider. Somewhere, something is always mispriced. Sometimes, it’s stupidly mispriced.

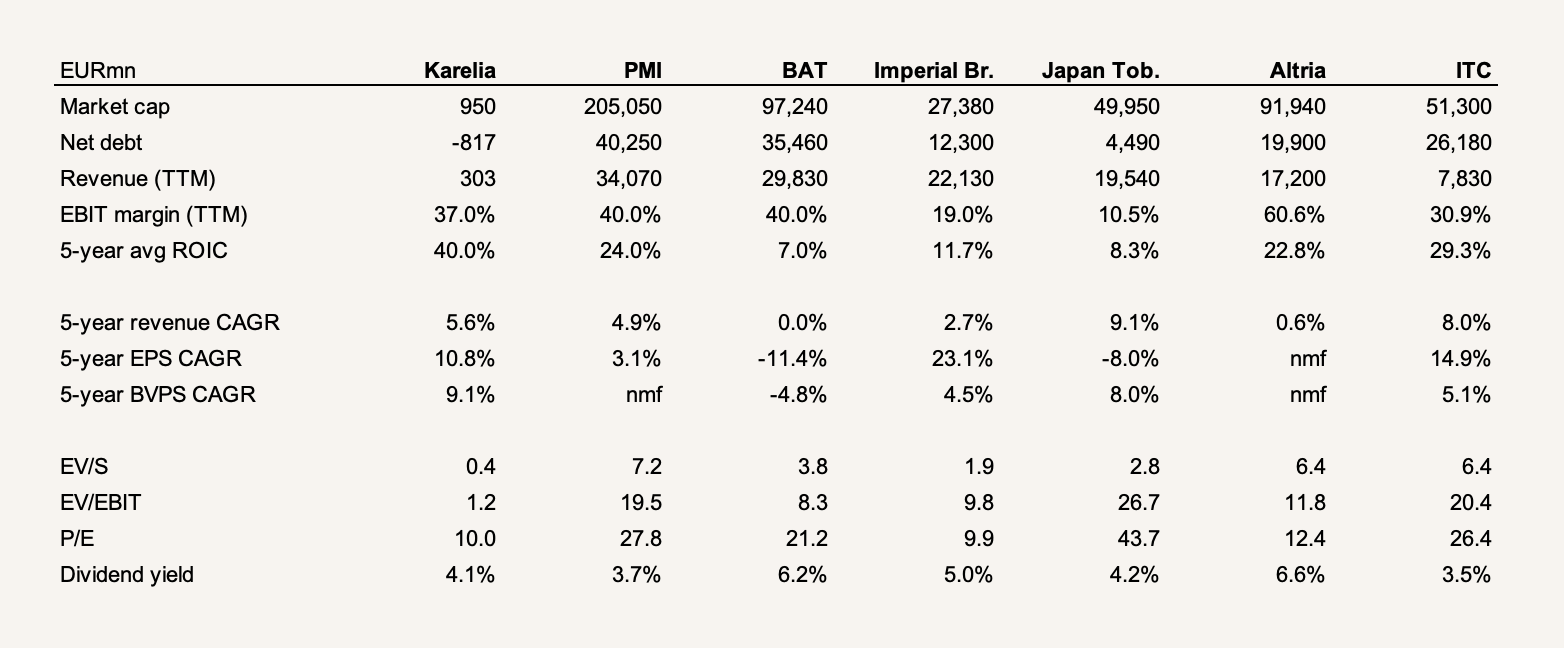

Karelia Tobacco sits about as far away from the AI-driven, growth-obsessed zeitgeist as you can get. It’s, and I apologize to the ESG crowd, a decidedly unsexy Greek tobacco company that’s been on my radar for some years. It’s also a name that’s circulated in deep-value circles for just as long.

And for good reason. Even as Karelia is likely the only listed tobacco company still putting up consistent volume growth in the structurally-declining world of cigarettes — a business that, for all its moral baggage, remains one of the most cash-generative, price-inelastic, high-returns consumer product businesses ever invented — the market steers clear. By any metric, the stock is cheap, even after compounding shareholder returns at ~16% annually since 2012.

But before you fall off your chair, as you realize that scarce stocks are actually mispriced because they’re overlooked (like this one), know that Karelia probably isn’t one of them. Because there is no shortage of reasons for the mispricing either. To many, the following make Karelia uninvestable and effectively repel institutional capital:

- It’s a tobacco company. The industry is thoroughly vilified, and ESG-driven mandates and divestments have drained the investor base. Many funds are outright prohibited from owning tobacco. It sits in permanent exile from polite capital.

- But even if funds wanted to own it, no fund that isn’t tiny or with permanent capital could do it anyway. With a float of ~4%, the stock is illiquid. Median daily volume over the past year is ~100 shares, and it comes in spikes. There are days with no trades.

- A Greek small cap is about as far from the MSCI comfort zone as it gets. The combo of geography and post-crisis risk premium is enough to stop most investors before doing further due diligence.

- It’s completely family-controlled. The Karelia family, split into two factions, owns ~95.9% of the shares. They call the shots, and minorities are along for the ride. Interim results have routinely been released much later than what’s normal for a publicly-listed company, and family disputes occasionally spill into governance. You probably guessed that investor relations are virtually non-existent. Only since FY22 have annual reports been delivered in English.

- With >EUR800mn of net cash and investments, or 86% of the market cap, the company functions as the family’s piggy bank. To outsiders, it looks like capital inefficiency, but to the Karelias, it’s insurance. They’ve watched Greece implode once and have no interest in any type of risk. That conservatism, though frustrating to investors, is also what’s kept the family in control since 1888 and the business remarkably resilient.

- Unlike Big Tobacco, Karelia hasn’t moved into smoke-free categories. It still makes only traditional cigarettes and rolling tobacco. That makes the stock ESG-unfriendly squared. Yet the company has quietly compounded, its strength lying as much in geography as in discipline. Its core markets — Greece, the Balkans, and more — are stable, regulated, and, crucially, still smoke with strong brand loyalty. Big Tobacco participates in these markets but pays far less attention to them as rounding errors in the books.

- With just one factory in Kalamata, Greece, serving all markets, there’s a key asset risk inherent in the business.

Every structural, behavioral, and optical headwind lines up to keep this thing ignored and mispriced for a long time. So why am I writing up Karelia now? For two main reasons, and both are recent events. I’ll give you the first one right away and spell out the other behind the paywall.

The first is that Karelia is cheaper than ever. With EUR817mn in net cash and investments, the market prices the enterprise at EUR133mn. (Most data providers miss this because a chunk of the investments sit under non-current assets.) The business made almost its entire EV in operating income over the past 12 months. In FY24, it made EUR105mn. In FY23, it made EUR97mn. In FY22, it made EUR103mn. Actually, over the past decade, Karelia has generated EUR91mn in average operating income with a standard deviation of just EUR9mn. The stock is priced as if the business is about to vanish.

From a financial perspective, tobacco is an infamously great business. Demand is habit-driven, pricing is inelastic, innovation is mostly unnecessary, gross margins are fat, and it’s capital light. It’s resilient through economic cycles, war, and whatever else, and established distribution networks add another layer of protection. Strict regulation, cast as a risk, doubles as protection from new entrants as advertising bans and compliance regulations entrench the incumbent market leaders. Philip Morris, before becoming Altria, was the best-performing stock in the S&P 500 between 1957-2003, compounding at 19.8% annually.

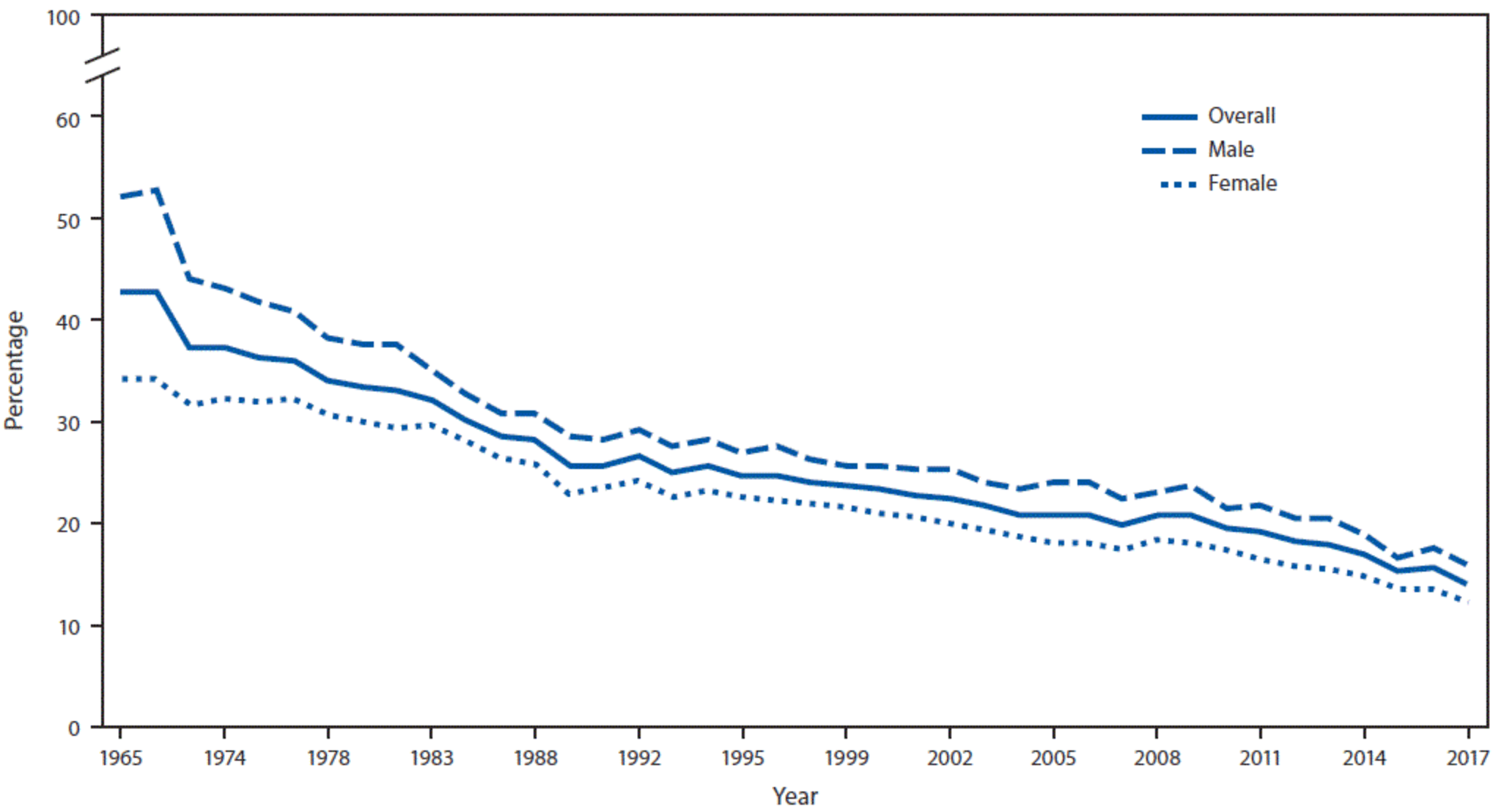

As everyone knows, it’s the changing habits that are the real existential threat to this business. Globally, that demand erosion has crept into Big Tobacco’s volume sales, slowly and predictably. What many don’t realize, however, is how long this has been happening. Cigarette consumption peaked in the 1960s, at the height of the Mad Men era, and the decline since has been surprisingly gradual.

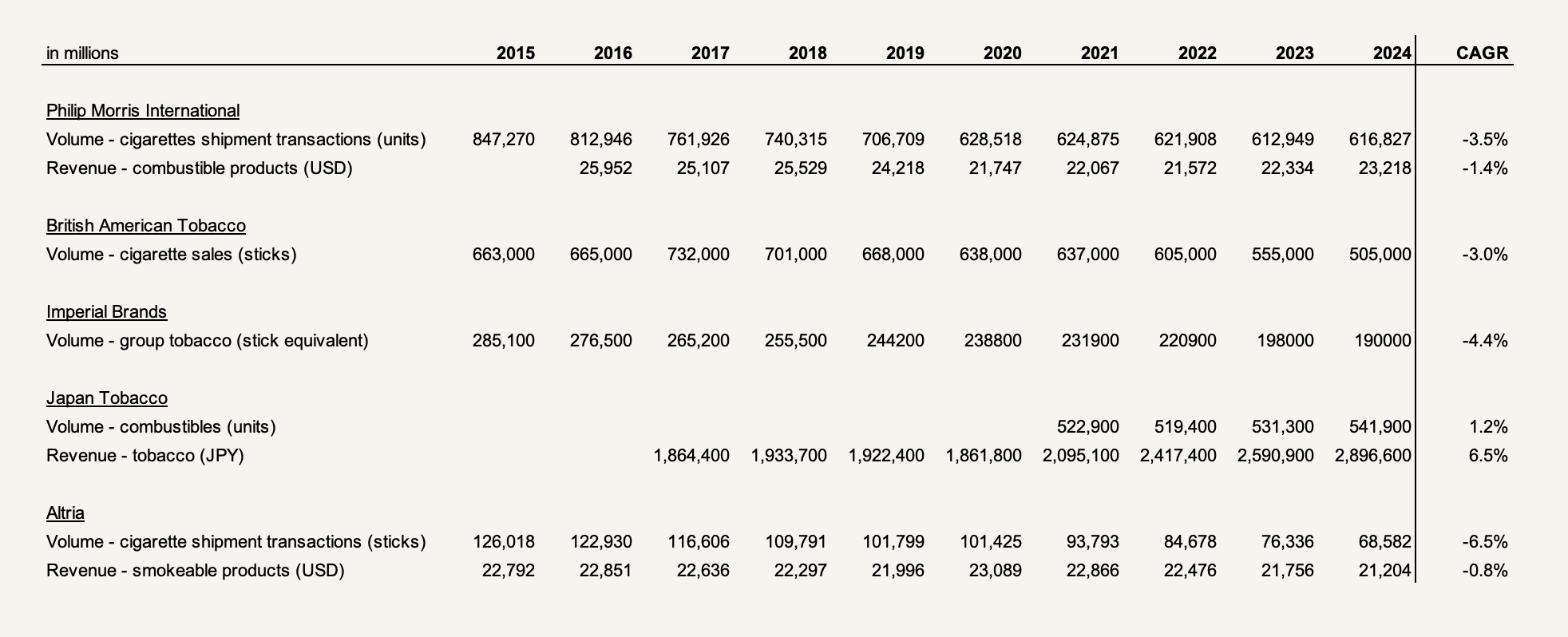

Here’s Big Tobacco’s cigarette volume sales from 2015-2024, showing a low- to mid-single-digit annual decline. Altria, with its full exposure to the U.S. market, has fared worse:

Yet, profitability hasn’t followed volumes down as the industry has been rescued by its pricing power over the pool of smokers remaining. As governments kept raising VAT and excise duties, Big Tobacco just passed them through, and then some, with that “then some” flowing straight to the bottom line. Lower volumes also meant less production and working capital, which in turn has supported higher owner earnings than reported earnings.

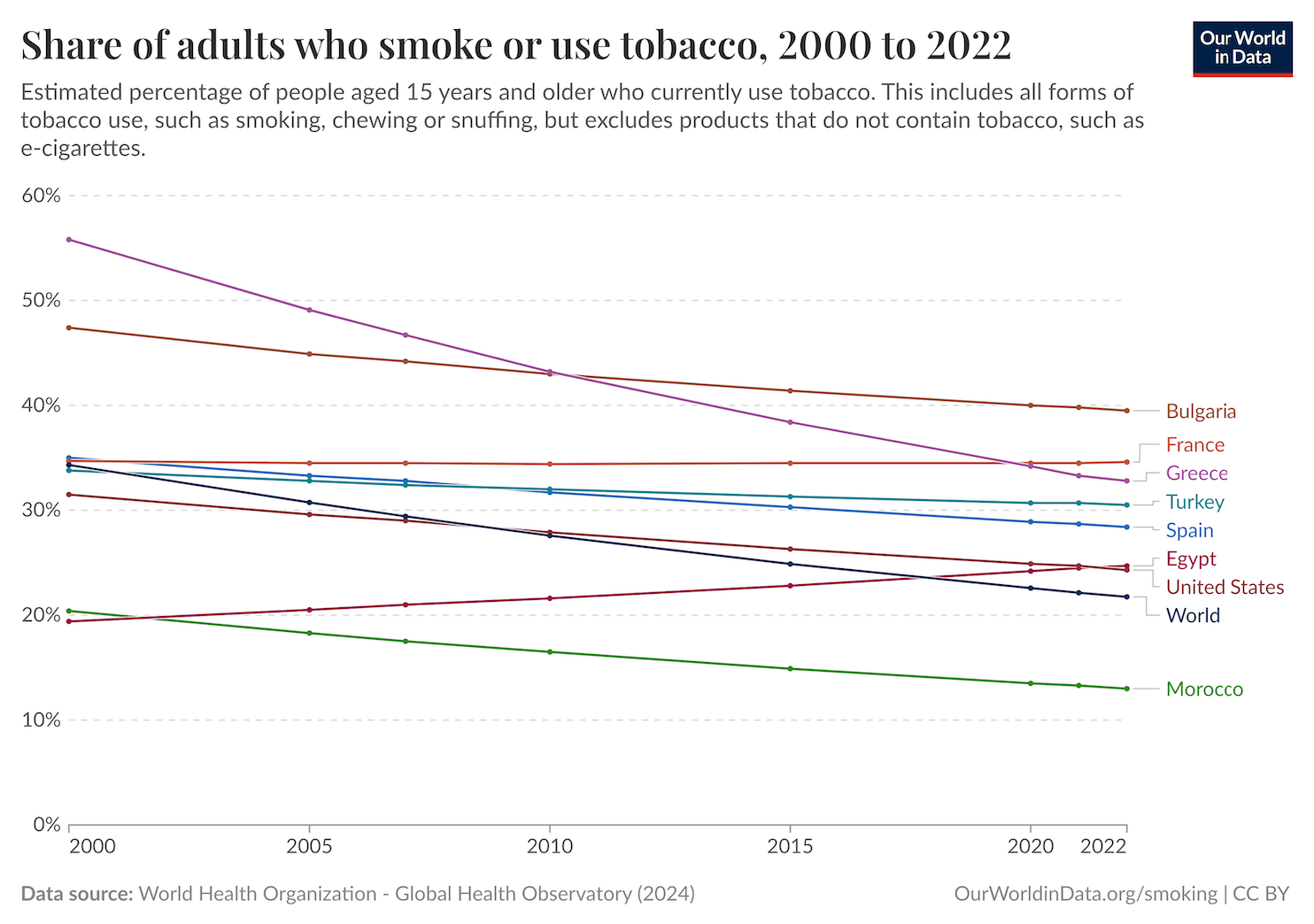

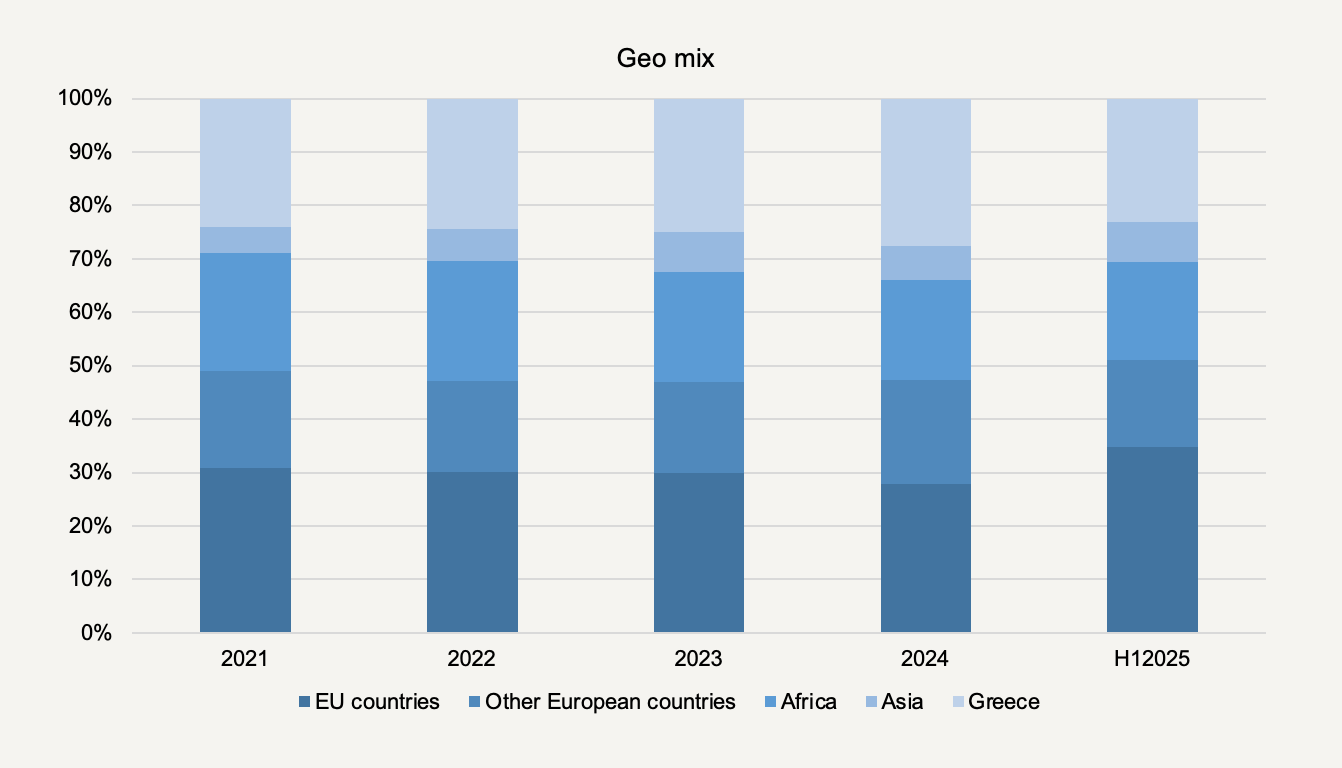

In Karelia’s markets, the picture above is flipped. Across its footprint — Greece, Bulgaria, other Balkan countries, Turkey, North Africa, and parts of Western Europe — volumes have, ostensibly, remained stable, even mostly growing. Cultural norms in Karelia’s parts of the world have been slower to change, enforcement of smoking bans has been inconsistent, and next gen products have gained relatively limited traction.

Or at least, that’s what I hear and read on the Internet. In practice, I have yet to find national data that confirms this narrative. (Smoking statistics are typically patchy, outdated, or methodologically inconsistent across many markets.)

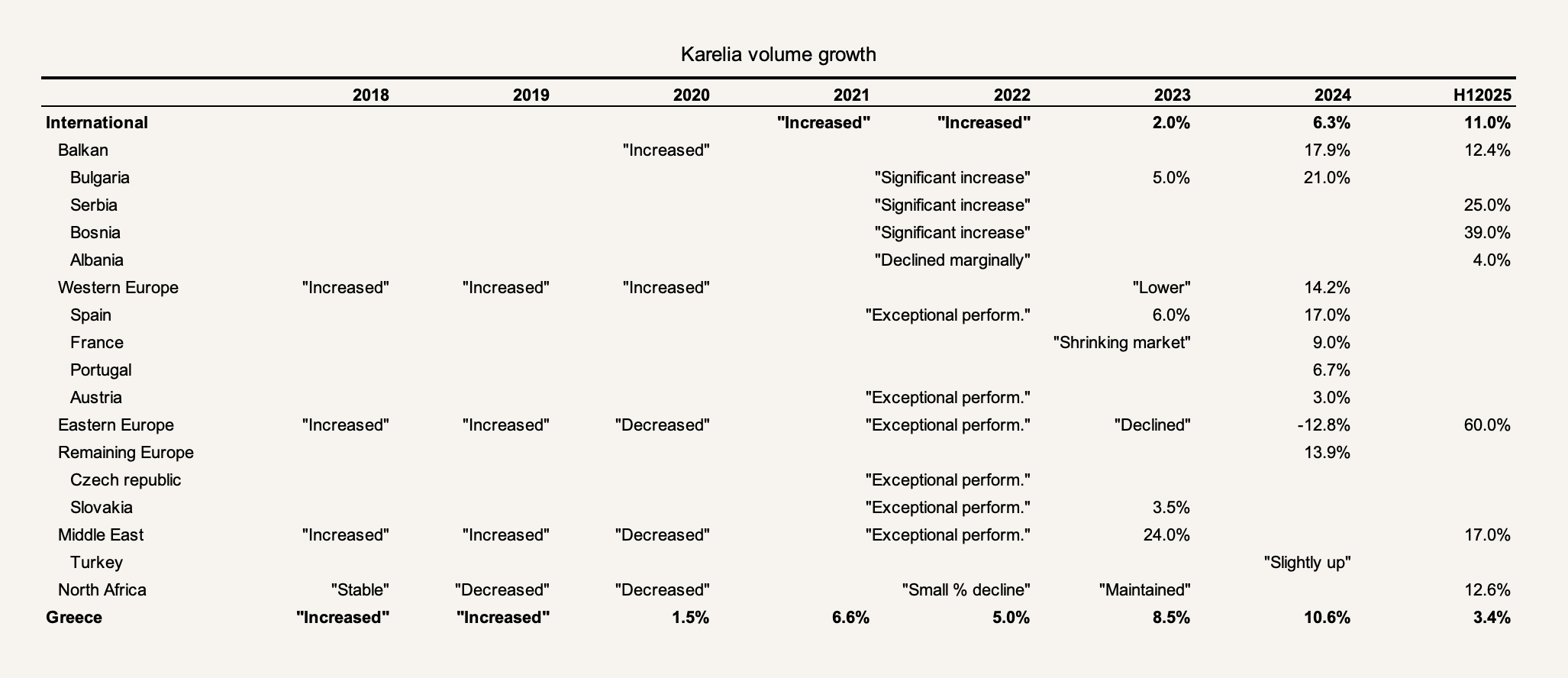

But I have gathered numbers and commentary from Karelia’s annual reports that confirms remarkably consistent volume growth, which means either national statistics are wrong, or that Karelia is quietly taking market share (it already holds >20% of Greece’s cigarette market). I’m happy either way (for the company). I know the table below is messy, but just glance over the lines for Karelia’s two geo segments, International and Greece, in bold:

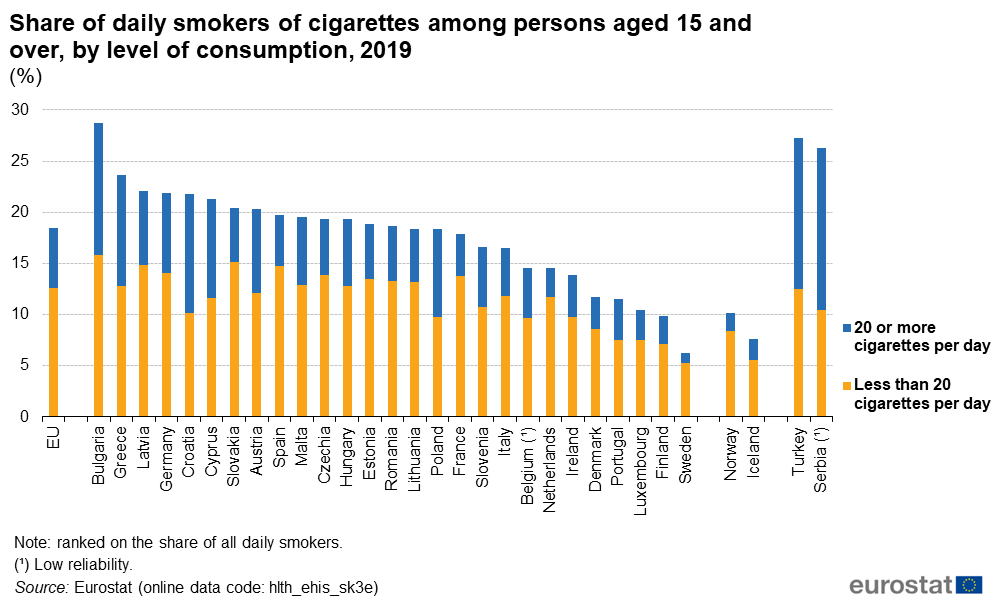

The distinction between price and volume growth matters quite a bit because smokers’ disposable incomes only stretch so far before downtrading or quitting becomes unavoidable. Volume growth, on the other hand, provides a still-expanding consumer base on which to exercise pricing power later. Since 2019, Karelia’s net revenue growth has closely tracked its volume growth, suggesting that it has yet to pull the pricing lever beyond excise increases. All else equal, that leaves some dry powder if consumption eventually plateaus. Both Greece and Bulgaria, meanwhile, sit at the very top of the EU in smoking prevalence.

It should be noted that while Bulgaria has among the lowest cigarette excise duties in the EU, supporting the statistic above, the Bulgarian government has raised excise duties twice in the past year. In Greece, Karelia expects intensifying competition from next gen products in the near term. Also, excise duties are an easy lever for politicians to fund increased defense spending and whatever else. So while volume growth in Karelia’s market will obviously not continue indefinitely, it merely suggests that Karelia’s runway in traditional tobacco is longer than for peers.

Volume growth is only really valuable if a business earns defensible returns on capital. But it goes without saying how great a business this is. With an EBIT margin in the 30s, fixed assets that turn over 4x at its modern and efficient single plant in Kalamata, and negative working capital, returns are so high that incremental growth is essentially free. The customer base is highly fragmented through a 26k POS network. Reinvestment needs are so low that FCFF stably runs >100% of NOPAT. In FY24, the company spent just over EUR1mn upgrading its plant and another EUR5mn on new production line orders, which just came online recently to support growth. This is just ~2% of its annual net revenue.

What I find interesting is that Karelia’s gross margin has compressed by ~4ppts since FY21, reflecting higher procurement costs for leaf tobacco, which has seen price increases due to supply shortages and a stronger dollar, spiced up by inflation in energy, transport, and packaging materials. Karelia’s selective approach and pricing discipline have absorbed part of that cost pressure, expecting these effects to normalize and the gross margin to shoot back up. This makes the enterprise value look even cheaper.

Now to the second, more important, reason why Karelia is interesting now…