Pricing power

…and how to identify it in its most durable form.

“We have found in a long life that one competitor is frequently enough to ruin a business.”Charlie Munger

A common mistake investors make is buying a stock based on what the company has done in the past even if that doesn’t translate into conviction for how the company may thrive in the future. The truism of stock investing is that you don’t buy a company’s past cash flows; You buy the future. But many investors incautiously buy widely popular stocks that have shown immense promise in recent years in perhaps an exciting new industry only to discover that the company fails to live up to those expectations set for the next 10-20 years taking into account the price paid for the stock.

The “exciting new industry” part is noteworthy since the two-folded mistake is trying to pick the right industry by assessing how much it’s going to affect society or how much it’ll grow. To the non-user of second-order thinking, there’s a reason why that approach is bound to disappoint.

There are industries, often new and exciting, that have little to no barriers to entry. The name of the game in such industries is that you need to run faster than the others. Of course, that’s exciting stuff because that’s where you’ll see the most innovation coming in with the hope of immense shareholder value creation. But this is often an illusion. Having to run fast is a long-term setup for failure. You’ll always have competitors looking at what you’re doing, trying to figure out your weaknesses, and waiting for the right moment to attack. Fat earnings invite others to come in and sample the cream. History is awash with companies experiencing rapid growth that ultimately burn through shareholder’s capital. The reason is: if supply outpaces demand and companies don’t have a moat, it doesn’t matter how fast demand grows—everyone except maybe the customer loses. Examples include railways in the Victorian era, automobiles in the 1920s, fiber-optic cable in the late 1990s, wireless networks in the 2010s (specifically in regards to new network upgrades that weren’t yet monetized), solar panels in the early 2010s, shale oil and gas in the 2010s, and more recently, cannabis and lithium. You even want to through some recent pockets of SaaS in there. Typically, stocks rise as investors anticipate a surge in demand only to fall later on when supply exceeds demand and losses accumulate. Industry is not destiny.

The key is not assessing how much an industry will grow but how its economics are divided between the players who possess durable competitive advantages that allow them to squeeze and forward the value to the shareholders. A company that has grown earnings recently but doesn’t give any clues as to whether they’ll grow consistently doesn’t have that ability, and buying the stock for those unknown earnings does little for you. The business may be well-run with great management that always does the right thing when its back is against the wall, and it may even possess an advantage that differentiates it from competitors to generate attractive profits, but since there’s no assurance that such an advantage will yield long-term protection of earnings power, it isn’t durable and thus holds little value to the investor. Short-term advantages are useful, but they shouldn’t be mistaken for moat-building.

As Michael Porter has said:

“It’s incredibly arrogant for a company to believe that it can deliver the same sort of product that its rivals do and actually do better for very long.”

So the difference between a moat and a competitive advantage is: an economic moat originates from competitive advantages (the more, the merrier), but for those advantages to merge into a moat, they have to be sustainable.

All this matters little to short-term investors and traders. The marginal buyer of a stock that aims to only hold it for a couple of months will not care much about the company’s moat, because the advantages that make up the moat won’t matter much over those couple of months. What matter over that period are market sentiment, news flow, and short-term momentum.

Because short-term temperament is an inherent trait of the stock market, there’s room for value creation in competitive advantages that last for years and years. In other words, companies with moats that are truly durable almost always trade too cheap since the vast majority of the company’s value lies in the outer years.

If you’re a banker doing valuations for a living, what do you do? You’re valuing one company after another, projecting into infinity for every company that comes across your desk. It’s shaky grounds and everyone knows it. The investment banker knows it. For the majority of valuations, the terminal is just a tie-up to the model. A valuation that assumes a cut-off to the terminal period is few and far between but that’s the reality of the business ecosystem. No company lasts forever. Some last a few years, some even for a few months, and some last for centuries. Some last for decades without creating any value. Only rare companies create value long enough for the present value difference between ‘very long’ and ‘infinite’ to become insignificant.

How many companies do you feel comfortable projecting five years into the future, then another five years, then another five years, all the way into infinity, with close to what’s real conviction? How do you know the prospects you’re projecting will all be value-accretive to shareholders? For valuations with little conviction, the terminal means nothing—perhaps from a learning perspective but not to make a qualified investment decision.

What’s the remedy? The first is to study lots of businesses—over a lifetime—and then if you’re lucky, you’ll find a handful of real moats you can confidently project with overwhelming odds. Studying company after company leads to predictability. The basis of that predictability is a wide moat around the business that protects it.

In moats, it’s easy to get symptoms and causes mixed up. We usually think of moats as something concrete to slap on a description of their origin. “This company has a moat because it’s capital-light, retains >90% of customers per year, and building its plant requires a gigantic investment by any new entrant.” Such descriptions are symptoms, not causes. It’s like Richard Feynman’s saying:

“I learned very early the difference between knowing the name of something and knowing something.”

Mixing up symptoms and causes runs the risk of dismissing moats in places where you don’t expect to find them, or, contrastingly, discovering moats where you do expect to find them but that are elusive or aren’t as wide and deep as you think. Southwest Airlines operates in a notoriously terrible industry burdened with gigantic fixed costs, a commodity product that earns its margins on the tail end, huge debt, and price wars with imminent bankruptcies to follow. But the context of these terrible industry economics is the source of Southwest’s moat-building at the expense of bloated/lazy competitors and the benefit of the price-conscious customers. Its cost discipline, plane agility, and standardized fleet are what flow into the differentiator for a commodity product such as plane tickets: low ticket prices. All the little intricacies and nuances are what make Southwest’s low-cost operator model work. This isn’t much different from the scale economies shared you see at the most successful retailers like Walmart.

So it’s sometimes a waste of time to analyze a company’s current product and market to assess its future value. When Amazon listed in the late 90s, even the most bullish analysts thought its TAM was $26bn which equalled the total US book market. What failed to be appreciated was Amazon’s adaptive, long-term culture that stampeded every factor you could have included in your ’90s analysis. That’s the important ingredient in moat-building: a culture willing to invest for the long term and a management unsympathetic to playing the quarterly circus of Wall Street.

Moats aren’t built out of thin air; they’re built by humans. What’s commonly overlooked are the incremental daily improvements that aren’t noticeable in the everyday financials but which slowly turn into formidable protection of the castle. A culture fanatical about the little daily improvements is the intangible glue that can keep growing businesses together, the facilitator giving space for innovation, and the reason why companies can emerge stronger from adversity. At the micro level, if the company is continuously delighting customers and eliminates unnecessary costs, its moat gains strength. If it treats customers with indifference or tolerates bloat, it’ll wither. Moats are not built and then stick. They’re always changing, either expanding or shrinking.

“If you’re See’s Candy, you want to do everything in the world to make sure that the experience of giving that gift leads to a favorable reaction. It means what is in the box, it means the person who sells it to you, because all of our business is done when we are terribly busy. People come in during theose weeks before Chirstmas, Valentine’s Day and there are long lines. So at five o’clock in the afternoon some woman is selling someone the last box candy and that person has been waiting in line with maybe 20 or 30 customers. And if the salesperson smiles at that last customer, our moat has widened and if she snarls at ‘em, our moat has narrowed. We can’t see it, but it is going on everyday. But it is the key to it. It is the total part of the product delivery. It is having everything associated with it say, See’s Candy and something pleasant happening. That is what business is all about.”Warren Buffett

When analyzing companies, two biases that can turn your research into mush is framing and the narrative fallacy. Like an attorney who selectively gathers evidence to build his hypothesis rather than viewing the case from multiple different angles, actively looking for moats and thus creating upbeat stories around a company risks falling prey to the same irrationality (which, from the attorney’s perspective, is misaligned incentives). If you approach researching a company with the goal of badly wanting it to have the moat you presume it to have, there are loads of cherished concepts you can easily pick and choose from to build your case. A large company with bunches of plants? That probably translates to scale economies. A well-known company with stores all over the country? That probably translates to a strong brand. Sears and Kodak are examples of brands that were easy to slap on a bunch of advantage stickers but which failed to adapt to changing market conditions so it didn’t matter.

Survivorship bias plays a role too. Just like nature, history, and ecosystems don’t agree with human conceptions of good and bad, but merely define good as that which survives and bad as that which doesn’t, only the surviving business tells the bigger story. History always fails to include important, variegated details, thus overexplaining the path dependence to an outcome. The territory isn’t the map. You can have two different companies of the same size employing the same strategy and having the same competitive advantage of scale and product stickiness, but one of them may trounce the other due to some singular, perhaps cultural, little factor that didn’t look so important at the time but turned out enormously important in hindsight. Merely explaining the winner using concepts like scale advantage, stickiness, and pricing power, may not be enough. By sampling only past winners, studies of business success fail to answer a critical question: how many of the companies that adopted a particular strategy succeeded?

It’s important to learn from case studies over synthesized concepts. When learning a business concept for the first time—and I think here about the overused concept of “flywheels”—you tend to take the concept at face value. You think that all you need are a couple of examples and then you can go put the framework to practice. Then you start seeing flywheels everywhere until you figure out that it never applies cleanly.

Business is an ill-structured domain. It’s messy and dependent on context guaranteed to be unique. A good analyst recognizes how they’re unique by having a rich backlog of studies and experiences to pattern match against. If you treat all moats made up of the same competitive advantage the same, you can’t know how deep and wide they are. Charlie Munger preached having a “latticework of mental models” in your head, but whenever he explained something, he did it through reasoning by analogy—analogies carried by a backlog from a lifetime of study. The more business cases you study, the more concepts you’ll have at your disposal. As you gain experience, you’ll become more equipped to draw accurate conclusions while avoiding preconceived notions, tailoring your approach to the specific situation, and including appropriate caveats.

No formula in finance tells you whether a moat is 28 feet wide and 16 feet deep. That’s what drives investors to dismiss their importance. They can compute standard deviations and betas, but they can’t understand moats. It’s always been the nature that intangible assets—the ones we can’t see or feel—are hard to quantify. When something is hard to quantify, accountants do a poor job of assessing its value, and therefore it doesn’t properly show up in the numbers.

Many moatsters will tell you that the only test you can conduct in assessing a company’s moat is whether its return on invested capital is above its cost of capital. While somewhat true, there are caveats:

So while the ROIC test is useful and should always be the ultimate, and eventual, yardstick for value creation, it’s not an exhaustive estimation of a company’s moat building. Here are other useful approaches to mix it up:

This is not a way to quantify a moat with absolutism but is a test of its durability. There’s a theory that you can’t truly know that a moat or entry barrier exists until that moat is attacked by a well-equipped competitor and the attack is repelled. Like evolution, capitalism is a brutal place. Companies attack other companies all the time. It’s just a matter of keeping your eyes open.

Facebook’s moat was tested in the early-2010s when Google launched Google+. Starting as project “Emerald Sea”, Google didn’t just want to invent a Facebook killer; It wanted to reinvent what it meant to share information on the web. And considering its monopoly in processing web info, how could it ever fail? There are many theories as to how they ended up failing after a decade of trying, including bad management, but the real reason is found in Facebook’s fierce management and sect-like culture. Google had lots of reasons to fail, falling back on the search engine as the cash cow; Facebook’s social network was all it had. So of course Facebook was ready for war. The week Google+ launched, Zuckerberg put Facebook into lockdown, not letting any employee out of the building until a strategy was put down. Whereas Google was slowly growing into a bureaucracy, Facebook was still entirely run by engineers led by a “hacker” ethos. If you could get shit done quickly, nobody cared about credentials or traditional legalistic morality. Facebook won the fight and Google+ was officially shut down in 2019. It wasn’t before Facebook was attacked by the mightiest competitor of them all, at five times Facebook’s size, that it exemplified Facebook as the definitive social network. It was also an example that Facebook’s moat at the time it mattered wasn’t just made up of network effects. Google+ was already built on the most entrenched network of all time (that between connecting users and advertisers on the web)—there was a Google Plus sign-up button practically everywhere across Google’s product, the product was simpler, and, subsidized by the Adwords cash cow, it showed no ads on the social platform—but Zuckerberg’s leadership and Facebook’s culture gave it the extra notch to win the war.

Adobe is another more recent example of the attack-and-repel test, although this one from disruption. Until Figma came along, Adobe’s moat was deemed impenetrable, having ridden almost three decades as the de facto standard in digital design. Figma changed the game by being browser-native and solving designers’ need for collaboration. The fact that Adobe finally attempted to acquire Figma for $20bln, or 100 times trailing annual recurring revenue, is a testament that you would need to update your assessment of Adobe’s moat’s width and depth. The attack-and-repel test became an attack-and-pay-up-to-get-us-out-of-the-way result.

“You give me a billion dollars and tell me to go into the chewing gum business and try to make a real dent in Wrigley’s. I can’t do it. That is how I think about businesses. I say to myself, give me a billion dollars and how much can I hurt the guy? Give me $10 billion dollars and how much can I hurt Coca-Cola around the world? I can’t do it.”Warren Buffett

Ask yourself how much it would cost you to take on the incumbent. Economies of scale often require that a new entrant or challenger needs to reach a minimum viable market share to be a viable competitor to the incumbent. For example, for a beverage business to sustain the distribution and marketing infrastructure it needs to compete effectively, it pretty much needs to reach a 25% local market share. A car manufacturer that prominently competes globally would need to reach 1-2% market share.

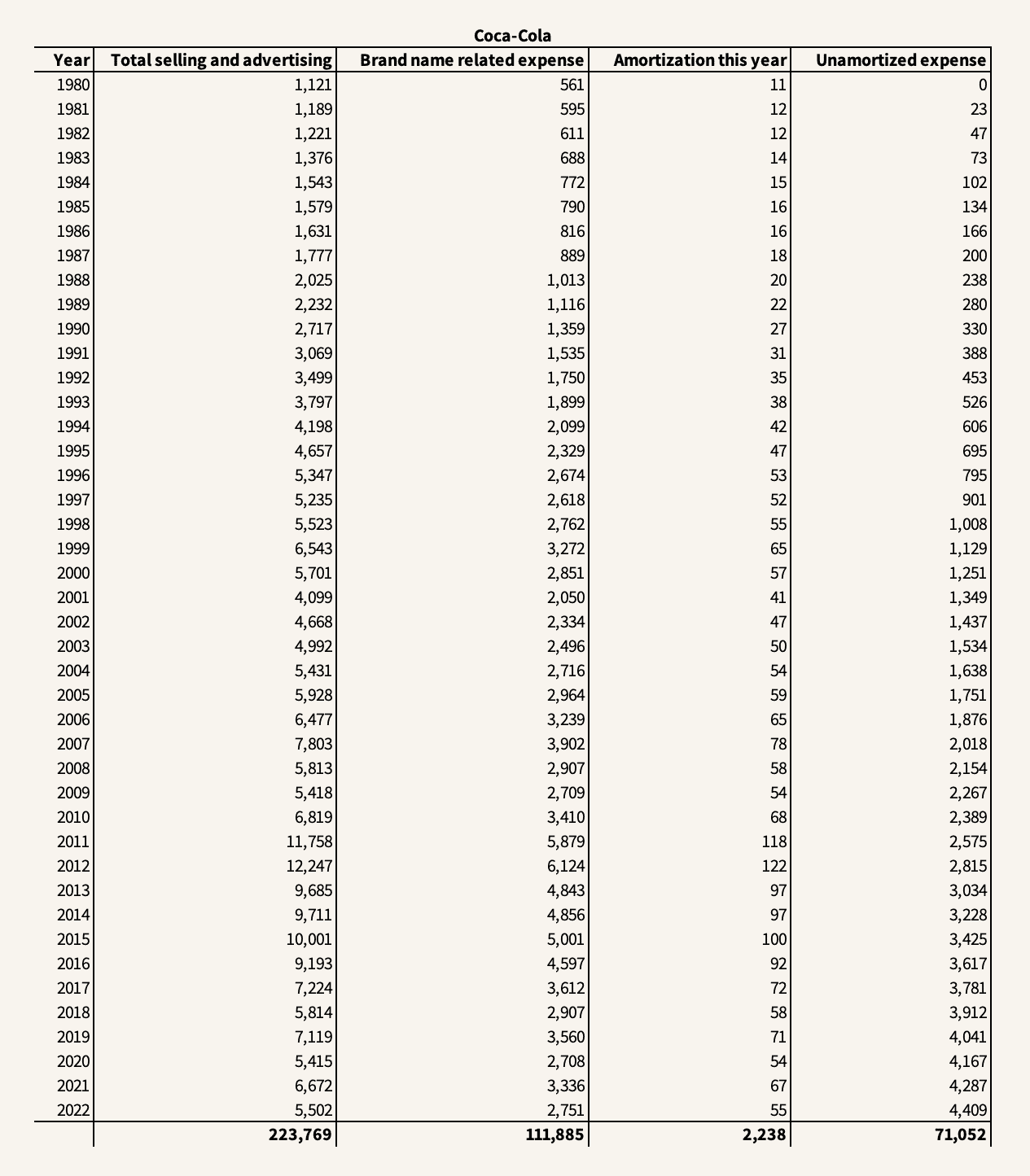

You could look at your company’s invested capital. But as I explain in the ROIC guide, many assets pass by the balance sheet, and destiny has it that the most important are often those that are directly associated with moat-building. With brand name, for instance, advertising expenses flow through the income statement, and therefore to estimate what a company has invested in its brand name, this would require looking at the company’s advertising expenses over time, capitalizing these expenses, and looking at the balance that remains unamortized today. But when you capitalize expenses, you also need to guess the right amortization period which is difficult and varies significantly by company. Of course, if a company’s moat is mostly made up of a patent, that’s an easy assessment, but with something like a brand, it requires you to intimately know the business (emphasizing the case study point earlier). Going all the way back to 1980, Coca-Cola has spent a total of $224bn on total selling and advertising. If we assume 50% can be attributed to brand-building, that’s $112bn. Now, to what degree can we assume that brand advertising spent in the 1980s still holds any value to Coca-Cola’s brand today? That’s a difficult question, but some of it might. Assuming a 50-year life of the brand asset, that makes for an unamortized balance today of $71bn. Does that mean it would take you a whopping $71bn to take on Coca-Cola? Perhaps.

This brings us to the second part of the equation: getting to a minimum viable market share may be elusive if the market position doesn’t last long. If the hands in the market shift too much every year (if the amortization of capital invested fizzles out sooner rather than later), spending all that capital may be value-destructive. So the second element regards velocity: how hard is it and how long does it take for the entrant to acquire the necessary market share? Industry stability—how much market shares change every year—reflects a host of factors, including customer captivity, proprietary technology, and so forth. A stable industry, where the hands rarely change, typically has inherent qualities of its incumbents that make it difficult for a new entrant to entrench the market. So if you have a company with a 25% market share in beverages, and the hands change 0.5%/year, you’re roughly looking at a 50-year moat (then you can take Coca-Cola’s market share viscosity and see that it’s probably more than a 100-year moat). Contrastingly, for a car manufacturer that has 1-2% market share in an industry where hands change a whole lot more, say 1%, that’s perhaps a 1-year moat, which is no moat at all.

The elevator & escalator industry is an oligopoly that’s remarkably stable and dominated by “the big four”. For a new entrant to get to a viable competitive position, it would probably need to reach >8% market share, which is difficult in an industry where sales are dominated by long-term service agreements of an already installed base that grows a measly 4-5%/year. Capturing 50% of new unit installations—and that’s already stretching it—would “just” accumulate ~15% share of the installed base over an entire decade.

On the contrary, the elevator business does not require a whole lot of invested capital since customers pay upfront for elevators and service agreements (negative working capital in both parts of the business) and elevator companies outsource production with only core technologies remaining in-house. In other words, there isn’t much scale advantage other than route density in the service market. So the elevator business does not require a lot of capital to get started, but it’s still diabolically hard to reach the scale necessary due to the viscosity of market shares that’s reflected in customer captivity and slow build-up of reputation. The elevator industry is one in which probably 0.5%-1% of market shares change hands every year, so you’re perhaps looking at moats for the major players that would last somewhere between 15-35 years. Incidentally, that may also approach the number of years a new entrant would need to get to a viable market share regardless of how much capital it’s willing to throw at it.

If you feel comfortable trusting Mr. Market’s prices (most of the time), you could do a relative valuation by taking the company that has a moat and comparing it to a company that doesn’t. If taking Mr. Market at face value doesn’t do it for you, you can DCF both companies and subtract the difference adjusted for size. The difference is the value of the moat.

Nick Sleep and Qais Zakaria used this idea at Nomad to quantify the size of a moat by looking at the amount of money a customer saved compared to the amount earned by shareholders. The criteria for the robustness ratio was that the value proposition was based on price, such as what exists at Costco, as opposed to an advertising-reinforced purchase such as Nike. Usually, that’s the prerequisite you see in businesses that are subject to scale economies. The formula is really simple: if customers in aggregate save $1bn compared to the next-cheapest alternative and the company earned $1bn as well, the ratio would be 1:1. One dollar saved by the customer equaled one dollar retained for shareholders. The basis of the robustness ratio is that the higher it is, the harder it would be to compete against the company on a like-for-like basis and it’s also predicated on the scale economies shared model that Costco uses to build its moat. When Nomad bought Costco, the ratio was 5:1. Five dollars saved by the customer equaled one dollar kept by Costco.

“A moat that must be continuously rebuilt will eventually be no moat at all.”Warren Buffett

Like the earth only orbits the sun for a finite amount of time, entropy makes sure all moats have an expiration date. Recent research has found that the time the average company can sustain excess returns is shrinking. Moats are shorter-lived. It’s a phenomenon not only attributed to high tech but is evident across a wide range of industries. Of course, the main reason is that technology has permeated pretty much every industry which has sparked a greater pace of innovation across the board. This phenomenon begs the question: are moats lazy, passive strategies that shun innovation? As Elon Musk once said in an earnings call: “I think moats are lame. If your only defense against invading armies is a moat, you will not last long. What matters is the pace of innovation—that is the fundamental determinant of competitiveness.”

But Musk’s claim isn’t new. Like the old David vs Goliath story, behemoths have always been attacked and overtaken by upstarts. The only thing harder than building a moat is not losing it when you have one. Oftentimes, poor strategic decisions or mismanagement are blamed when a moat is filled with sand, but there are other mental models, including game theory, that may help explain why moats die even in the midst of management’s best intentions.

In The Innovator’s Dilemma, Clayton Christensen distinguishes between sustaining and disruptive innovations. Sustaining innovations foster product improvement and operate within a defined value proposition. It’s about continually improving the company’s current value proposition, always providing more value to the customer than they pay for. Disruptive innovations, on the other hand, approach the same market with a different value proposition. They are divided into two types: low-end and new-market. A low-end disruptor offers a product that already exists but at a lower cost or with greater convenience, though typically inferior (think Southwest). A new-market disruptor, on the other hand, appeals to customers who weren’t even part of the incumbent’s main customer pool (think Uber).

Companies with moats usually aren’t lazy, failing to see what’s happening around them. They’re always engaging in sustaining innovations through continuous improvements of the product or customer experience. Otherwise, they wouldn’t have a moat in the first place. It’s the disruptive innovations that cause trouble, even if management is rational about responding to the threats.

For example, Christensen uses the example of mini-mills vs integrated mills in the steel industry in the 1970s. Integrated steel mills, which used blast furnaces to produce high-quality steel, enjoyed a significant advantage over mini-mills, which melted scrap steel and could only produce inferior quality steel. It was an unfair fight. So what the mini-mills did was they initially focused on producing rebar, used to reinforce concrete, which was also the least attractive and cheapest market for steel. When the mini-mills became too numerous, the integrated mills exited the unattractive rebar market and as a result saw profit margins soar. However, by concentrating on making the best rebar production possible, the mini-mills gradually improved their technology, enabling them to make better steel and penetrate more profitable markets. Over time, and slowly, the mini-mills entrenched the integrated mills and destroyed their profitability. As Christensen noted, the integrated mills’ decision to exit the rebar market felt good initially but ultimately proved short-sighted. The moral of the story is that managers of the integrated mills arguably made a perfectly rational decision of disregarding a market that offered lower margins, was insignificant to the larger steel market, and wasn’t in demand by the company’s most profitable customers. They listened to their customers and practiced conventional financial discipline, but were disrupted anyway.

If an incumbent faces sustaining innovation, it isn’t in much danger assuming its moat is strong. If a new entrant comes along with a sustaining innovation, incumbents are highly motivated to defend their turf and, as Christensen suggests, it’s rare to see an incumbent lose this battle to a challenger. But as in the case of the mini-mills, once the challenger is a low-end disrupter in what is already an unattractive market for the incumbent, the motivation is generally to flee that market. Likewise, if it’s a new-market disruption, in which there isn’t any proof-of-market and returns on capital spent, the incumbent will be motivated to disregard the threat. Considering the incumbents’ many options for capital allocation, including buying back shares, it can’t keep throwing money around at every potential disruptive threat since for every succeeding innovation, there are probably hundreds that wouldn’t succeed.

So the idea is to operate in a field that’s less prone to disruptive innovation. The Lindy effect plays a part here. If a company gains a moat quickly, it’ll have to worry about losing it quickly too. When an industry is unstable, the hands trade fast, even for the players deemed safe. Google’s search engine, one of the biggest profit pools in history, is an example of a mighty moat that’s obvious to everyone. But it’s also a moat that’s only a little over 20 years old, a fraction of something like Coca-Cola’s moat. Now GenAI is going to show how impenetrable Google’s search moat is. For Google to respond to disruption and perhaps let go of a technology and business model that has pumped out profits consistently for two decades is truly an “innovator’s dilemma”.

When looking for moats, resist overprescribing the types of competitive advantages that follow. Reality is more nuanced than single competitive advantages and other important factors are hidden behind the narrative. Brands are an example here as they’re commonly considered a strong foundation behind a moat. But some of the most well-known global brands, and I’m thinking of many consumer car brands here, consistently earn below or barely earn their cost of capital because they have no pricing power or emotional connection. There’s weak correlation between brand ranking and economic return in that industry. A moat is a rare creature and requires many advantages moving synchronously in the right direction. It’s what Munger called the Lollapalooza effect. Another rule is that no single competitive advantage works in moat-building if the right culture isn’t there.

Patents

Patents allow innovators to protect their innovation. Patents do not discourage innovation, but they do deter entry for a limited time into activities that are protected. Patents can be used as cynical moat-digging campaigns as long as they last, but once they expire, it’s gone.

Tariffs

Tariffs can be advantageous for companies in industries where there is significant international trade and where tariffs are imposed to protect domestic producers.

Regulation

While regulation can create challenges for companies, it can also create a moat by making it more difficult for new competitors to enter the market, giving established players a competitive advantage.

Licensing

Some industries require a license or certification from the government to do business which can be costly and time-consuming to get.

Standards

Macro-wide standards can be self-reinforcing, meaning that all the business sometimes accrue to the largest players. It’s related to network effects. For example, a debt issuer has little choice but to pay Moody’s for a rating if it hopes to get a fair deal in the market.

Ownership of scarce resource

Ownership of a scarce resource may cut off competitors from the same opportunity. After WWII, aluminum producer Alcoa signed exclusive contracts with all of the producers of high-grade bauxite, an essential material in aluminum production. But other than land and raw materials, a scarce resource could also be a distribution channel. For example, Salesforce has exclusive integrations with Google Analytics 360. In turn, Google pays Apple $16-20bn/year to be its default search engine.

Contracts with customers

Companies can secure future business through long-term contracts that may lock the customer for years but have the added benefit of reducing search costs for both the supplier and the customer. In the 1980s, Monsanto (NutraSweet) and Holland Sweetener Company both produced aspartame, a sweetener. When the aspartame patent expired in Europe in 1987, Holland entered the market and competed with Monsanto, leading to a 60% decrease in aspartame prices and losses for Holland. However, Holland had its sights set on the U.S. where the patent would last until 1992. To gain an advantage, Monsanto signed long-term contracts with the biggest buyers of aspartame, Coca-Cola and PepsiCo, effectively excluding Holland from the U.S. market. Here’s the important lesson: buyers may want multiple suppliers, but they may not use them.

Contracts with employees

Non-competes and NDAs can be sources of advantage for companies operating in industries with skilled labor.

Economies of scale are critical and often the driver behind the rest of the competitive advantages through feedback loops. But economies of scale can also be explanatory for how some moats die through bureaucracy, complexity, or input scarcity. As there are scale advantages, there can also be scale disadvantages.

Learning curve

The more you do something, the better you get at it, and the cheaper you can do it. The learning curve is particularly relevant for businesses with high fixed costs but is also affected by factors such as divisibility, such whether production can even be scaled (if a bakery wants to service a new region, it must open a new bakery, add trucks, and hire more drivers), complexity, like whether processes can be imitated, and rate of change in process costs, like whether costs can decline over time as a result of technological advances (the cost of building an e-commerce store today is negligible compared to twenty years ago).

Sunk costs

High exist costs discourage entry from new entrants. If getting into a business requires a huge investment with specified assets, these sunk costs can act as an advantage for the incumbents.

Economies of scope

When a company reaches a certain scale, its size can enable it to grow horizontally rather than vertically while achieving synergy between its horizontal activities. For example, there can be significant spillovers from R&D. When Pfizer sought a drug to treat hypertension, its research led it to think it might treat angina, but then found the unusual side effect which led to the blockbuster drug, Viagra.

Advertising

Some advertising channels, like TV throughout the latter half of the 20th century, are more efficient at scale. When TV came in, companies with strong brand names prospered.

Reputation

Reputation is built slowly over time and can be one of the strongest moat foundations besides culture. It’s subject to economies of scale because a strong reputation feeds on itself. It can also take the form of a cynical reputation. If a company gains a reputation for being ruthless and ready to fight at the least provocation, it can deter the competitor from attacking.

First-mover

Being first to reach minimum viable scale can either make it or break it for a company, especially if it’s operating in a winner-take-most industry.

Critical mass

Related to the first-mover advantage, once a company has reached a certain minimum viable scale, it may be significantly harder for a competitor to reach the same scale because the spot has already been filled. Critical mass is especially foundational to moat-building when coupled with network effects.

Bargaining power

Scale often means power over suppliers and can allow a company to source cheaper. Kellogg’s and Campbell’s moats have shrunk over time because superstores such as Walmart have grown. However, bargaining power may also provide some value to the supplier. Large firms are lowering their supplier’s opportunity costs by providing the supplier with better demand information.

Data

Tied strongly to switching costs, a data advantage sometimes makes it hard for a company or individual to switch vendor. For example, people who use Spotify and listen to lots of different music may find Spotify’s algo recommendations from thousands of hours listened so useful that they would never consider switching to other music software.

Capital

Access to capital, or an ability to raise it, is an advantage for companies in industries where capital is continuously needed to fund growth. The advantage is especially useful in times of distress since access to capital may allow making significant strategic decisions or acquisitions that reinforces the moat as lesser able competitors get wiped out.

Trade secrets

Companies may choose to keep trade secrets instead of filing patents, especially in the case of software companies where publishing algos can make it easier to copy. However, this strategy can leave the company vulnerable to competitors who could patent the same invention and sue the original founder for infringement. While trade secrets can allow litigation against employees who leak confidential information, it does not provide legal protection against competitors. There’s a nice case story named “Wohlgemut’s secret” on trade secrets in John Brooks’s book, Business Adventures.

Human capital

A shortage of skilled labor can be a significant advantage if you’re a company that has a strong workplace reputation and rigorous hiring process like Goldman Sachs or Alphabet.

Tacit knowledge

The difficulty of copying knowledge calibrated through experience and lots of feedback loops is like trying to masterly play the piano by watching someone else’s fingers move. Information theory and the closely related field of thermodynamics describe how easily patterns tend to gravitate toward disorder and information loss. Tacit knowledge is subject to conditional entropy through transmission. Therefore, companies having a significant knowledge advantage have little risk of losing it unless they lose their human capital.

Company culture

You know your culture is powerful when competitors know what you’re doing, and how you’re doing it, but they still can’t copy it.

Innovation

Only the paranoid survive.

Leadership

If culture is the machine of the company, leadership is the machine operator. When evaluating management it’s important to separate process from outcome. Having a good process doesn’t guarantee a positive outcome since many factors such as luck, competition, and technology can influence outcomes. Therefore, it’s better to evaluate management based on the processes they use rather than the outcomes they achieve in the short term.

Proprietary value chain/network/technology

Amazon is a moat builder through proprietary value chains and networks. The company’s proprietary value chain spans anywhere from the design and development of its hardware from (Kindle, Alexa devices, and the Graviton data processor chip), to its own logistics and delivery network (Amazon Prime and Amazon Flex), to its cloud computing services (Amazon Web Services).

Switching costs

Switching costs can arise from many sources, including contractual commitments, durable purchases, brand-specific training (a good one), information and databases, specialized suppliers, loyalty programs, and so forth. Bloomberg’s moat in financial data software is reinforced by the extensive training financial professionals undergo, starting at university, to learn the Terminal. Habit is a strong contributor to switching costs too. Bank customers rarely change their primary account which makes it difficult for large banks to steal business from small banks despite having scale advantages.

Search costs

Related to switching costs, search costs are largely attributed to experience goods that may be technologically complex. For example, Aspen Technology, a software business that offers process optimization to the energy, chemicals, and engineering industries, helps enterprises optimize their manufacturing processes, reduce costs, and improve efficiency which heavily reduces their search costs. And once the enterprise has invested in AspenTech’s software and deeply integrated it into its manufacturing processes, it’s not easy to switch.

Specialization

The killer of scale advantages is specialization. Munger once wrote: “We are the largest shareholder in Cap Cities/ABC. And we had trade publications there that got murdered—where our competitors beat us. And the way they beat us was by going to a narrower specialization. We have a travel magazine for business travel. So somebody would create one which was addressed solely to corporate travel departments. Like an ecosystem, you’re getting narrower and narrower specialization. Well, they got much more efficient. They could tell more to the guys who ran corporate travel departments. Plus, they didn’t have to waste the ink and paper mailing out stuff that corporate travel departments weren’t interested in reading. It was a more efficient system. And they beat our brains out as we relied on our broader magazine. Occasionally, scaling down and intensifying gives you the big advantage.”

Tradition

The durability of tradition mustn’t be underestimated. Famous for its traditional Chinese liquor baijiu, Kweichow Moutai, which at one point was China’s most valuable company, has built a moat rooted in Chinese tradition with a history that spans more than 2k years.

Location

Related to economics of density, a locational advantage can either derive from ease of availability or from achieving route density in operations by having locations, whether that’s plants, retail stores, or distribution hubs, close to each other. By aggressively targeting high-traffic, convenient locations, McDonald’s has a large locational advantage on a global scale, blocking competitor’s ability to secure equal prime real estate.

Brand

Compared to something like patents, brands are more fragile. However, they don’t have a fixed expiration date. A brand becomes valuable once it becomes share-of-mind. Buffett once said that Eastman Kodak’s moat was just as wide as Coca-Cola’s. “They are promising you that the picture you take today is going to be terrific 20 to 50 years from now about something that is very important to you. Well, Kodak had that in spades 30 years ago, they owned that. They had what I call share of mind. Forget about share of market—share of mind. They had something—that little yellow box—that said Kodak is the best. That’s priceless.” But time showed that Kodak’s brand moat had an expiration date: “They let that moat narrow. They let Fuji come and start narrowing the moat in various ways. They let them get into the Olympics and take away that special aspect that only Kodak was fit to photograph the Olympics. So Fuji gets there and immediately in people’s minds, Fuji becomes more into parity with Kodak.”

Network effects

There are two types of networks: a hub-and-spoke network, where a hub feeds the nodes (examples include most airlines and retailers), and an interactive network, where the nodes are either physically or virtually connected (Visa and Mastercard). Network effects do exist in the former but can be vastly more explosive in the latter.

Complimentary assets

Not all business relationships are based on conflict. Sometimes, companies outside the purview of a firm’s competitive bubble can heavily influence its advantages. Electric car manufacturers and charging station makers are examples of complementors. The value of both EVs and charging stations increases as there are more charging options. The more electric vehicles there are on the road, the more valuable charging stations become.