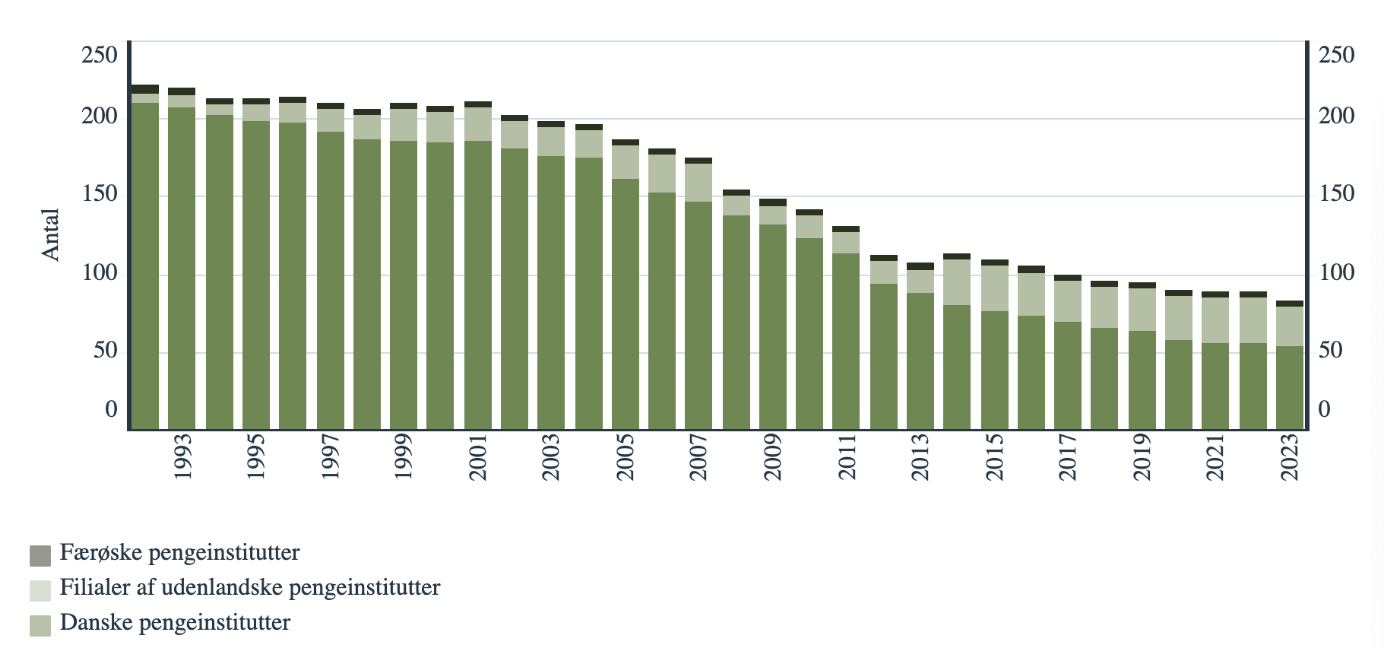

Denmark is overbanked. Although the number of banks in this tiny Scandi country has dropped from 219 (with 2.5k branches) in 1991 to 55 (with ~700 branches) in 2024, the four largest Danish banks hold nearly 90% market share. This compares to something in the mid-70s% in other European countries and <50% in Germany. It means that >50 of Danish banks are fighting over <10% of the deposit market. The shift from an agri-based economy to a service-based economy has shrunk the number of banking institutions for decades, and this trend is unlikely to end soon since Denmark still has twice the banks per capita as the European average. Of the 55 Danish banks, 18 are publicly traded. Consequently, most of the consolidation story remains out of reach for public market investors. But once in a while, you get an opportunity.

(Most of the following graphics will be in Danish. Here’s a nice source for Danish bank merger history.)

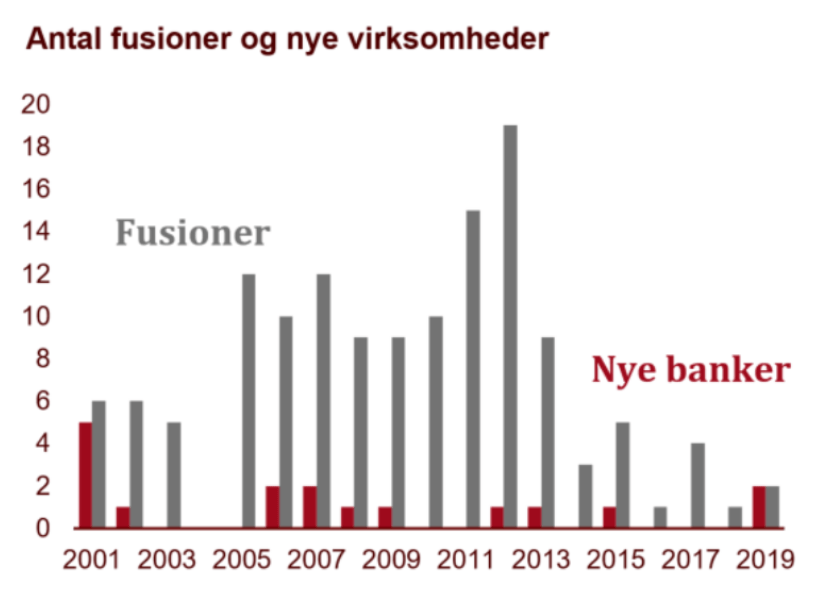

Compared to many other industries, bank mergers are relatively easy to execute, with rationale on both sides of the table. Community banks face a double-edged sword: they foster loyalty but lack scalability. Rising IT costs, compliance burdens, and increasingly complex regulations pressure small community banks to merge or get swallowed up to gain scale economies.

Because the lending side of banking is a commodity business, and the deposit side is where a low-cost advantage is to be gained (both in the deposit rates and the net non-interest expenses required to maintain those deposits), scale fosters profitability and serves as a barrier to entry. A study by Denmark’s competition authority, Konkurrence- og Forbrugersstyrelsen, shows that new entrant banks’ assets typically remain unchanged within their first four years of entrance, indicating mechanisms that limit entrants’ options for grabbing share.

These scale economies are largely related to IT and regulatory overhang. Banks face extensive compliance regs that are complex and require minimum levels of admin capacity, increasing fixed costs and competency requirements for staff. Meanwhile, smaller banks typically use standard models for capital adequacy, whereas larger banks are often permitted to use Internal Ratings-Based (IRB) models, which, all else equal, require lower capital reserves.

This is an industry that grows with nominal GDP — as its literal facilitator — and while most bankers would prefer to grow above this rate organically, it’s rarely feasible. Lending is extremely competitive, and it’s hard to reach for organic growth in a loan book without compromising asset quality. And with retail customer mobility in Danish banks averaging 5%/year (and that’s high attrition in an international context), unchanged for the past decade, it’s costly and risky to steal customers from competitors. So, dealmaking is necessary to elbow your way into a new turf.

From the seller’s perspective, getting swallowed up or merging has rationales too, especially if the bank is sub-scale, shareholder-friendly, and/or led by an ageing CEO or Board. This holds true even if the bank is led by incompetent management, as underperforming assets are often hindered by inept management rather than the assets themselves. Banks operating below their potential are ripe for acquisitions, rich with synergies. An acquiring bank’s core IT system and staff can often handle double the transactions at a small incremental cost. Additionally, a merged bank only needs one CFO, one marketing officer, and one risk officer, giving significant salary cost cuts. Skilled acquirers unlock further value by improving product pricing (such as rationalizing deposit costs), boosting non-interest income (acquirers, usually being larger, will cross sell their more expansive menu of products and services), and eliminating unprofitable or risky product lines.

The ideal target has, other than an attractive price, a low-cost deposit base with high DDA balances (indicating a moat), coupled with high G&A (indicating fat to be cut) and a geographic footprint that borders but doesn’t overlap with the acquirer’s.

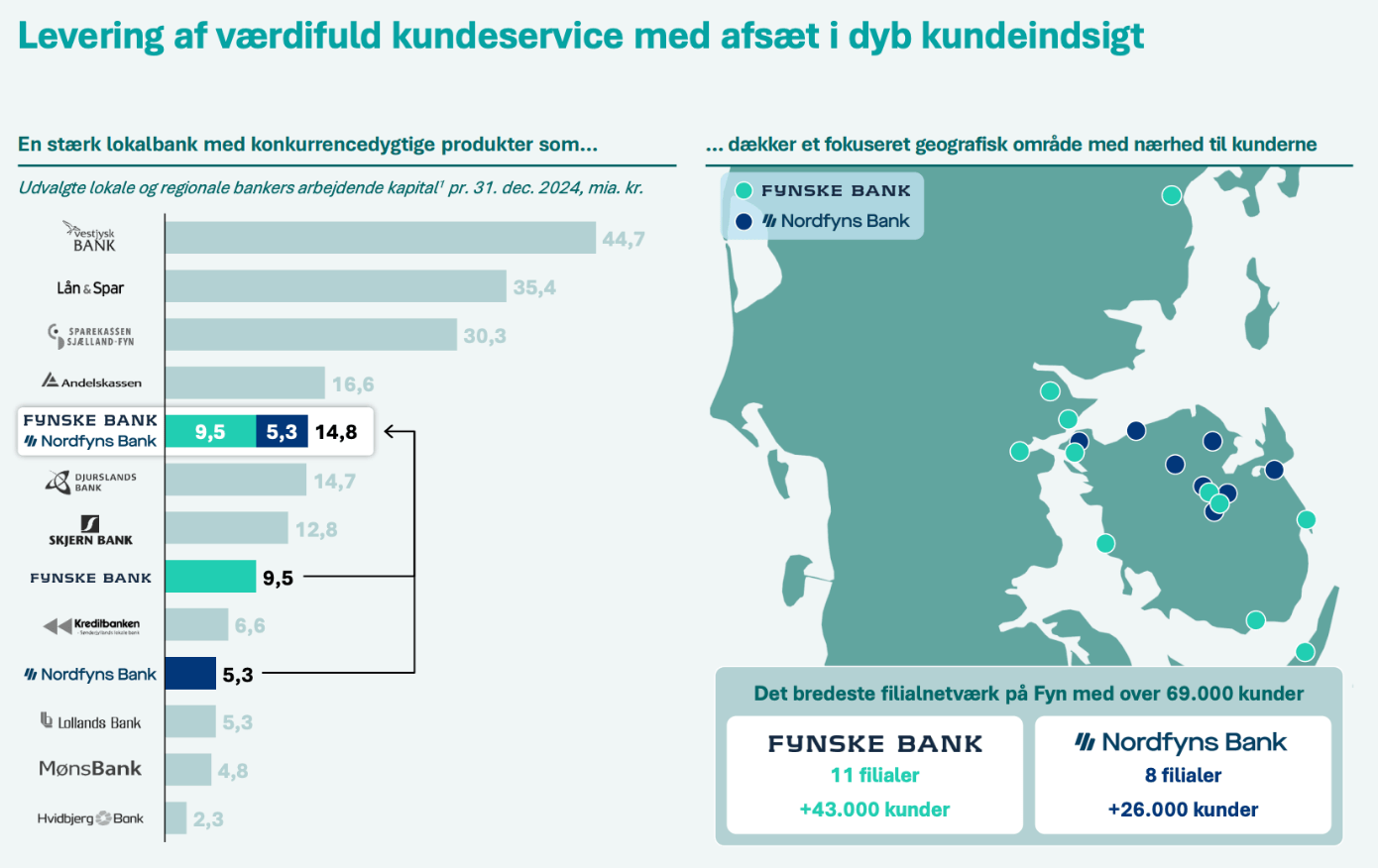

With a solid deposit base burdened by high central costs, this was the case with Nordfyns Bank, which just over a month ago planned to merge with its larger regional peer on the Danish island of Fyn, Fynske Bank.

It looked like a great setup. With a combined 19 branches, the merger would create the largest Group 3 bank and one of the country’s leading locally anchored banks, with DKK15.3bn in assets. Annual pre-tax synergies of DKK68mn, offset by DKK135 pre-tax one-offs, were promised, leading to a 13% slash of the collective cost base and a 66% pro forma cost-income ratio. Since the banks used different bank centrals — Bankdata and BEC, two of Denmark’s three providers — the majority of these savings would be crystallized by just paying a break fee to terminate one contract and migrating onto the other, with the rest coming from duplicated central costs and natural staff attrition. And while both banks were based on Fyn, their geographic overlap was minimal:

Nordfyns Bank shareholders were offered 2.7 shares of Fynske Bank for each of their shares, equating DKK378/share at the announcement — a 15.2% premium. In the weeks following, Fynske Bank’s share price ticked up, pushing up the offer price, but Nordfyns Bank’s share price climbed even higher, moving from a pre-announcement P/B of 0.7x to 1.1x. Even as the deal was cleared by everyone — the Boards, their representative assemblies, and competition authorities — requiring only a two-thirds shareholder vote to proceed, Nordfyns Bank shareholders saw the offer and upped the stakes by bidding the share price to a 10% premium over the offer. As the extraordinary general meeting approached for a vote, larger shareholders, including SJF Bank with 25% of the shares, publicly denounced the deal. Ultimately, on June 16, Nordfyns Bank cancelled the extraordinary general meeting due to “insufficient shareholder support”.

With an offer below book for Nordfyns Bank — a bank that achieved a pre-tax ROE of 16.1% on 7.5x A/E in FY24 — all synergies would have accrued to the acquirer, which is unusual in M&A. It certainly didn’t help when this article in FinansWatch hit the tapes reporting that Nordfyns Bank could have secured a higher bid from other buyers, yet the Board still urged shareholders to pull through. Thinking of why on earth insiders would want to do that, their incentives weren’t aligned with shareholders (at smaller, closely-held banks, it’s more likely that management will treat the bank as their own, even without owning the majority of shares). The merger agreement promised job security for all employees, including management, in the merged bank, which would employ 350 people (plus all of their representative assemblies counting 64 people). The merger could have been a defensive move to prevent a more hostile bid from the likes of SJF Bank or Sydbank, which owns 20% of Fynske Bank, where insiders would have less control over the process and outcome. Furthermore, there’s a strong link between a bank’s asset size and the compensation of its officers and directors. While Fynske Bank would be the surviving name and its current CEO, Henning Dam, would take the CEO job, Nordfyns Bank’s CEO, Holger Bruun, would, despite being demoted to bank manager, get a pay raise. None of Nordfyns Bank’s insiders, except Chairman Per Maegaard, hold any significant stake in the company.

Btw, selling out on the cheap isn’t exactly fitting with this quote from the annual report:

“Nordfyns Bank’s overall strategy is to remain an independent and competitive bank with a view to creating the greatest possible return for shareholders, to be a good and attractive workplace and to ensure high customer satisfaction through a focus on presence, commitment and competence”

With the deal off the table just days ago, two questions arise: 1) What are the potential acquisition scenarios from here, and 2) what are Nordfyns Bank shares worth?

Starting with (1), as the merger talks opened for the Danish bank consolidation narrative and triggered various commitment and consistency biases inherent in such processes, this is likely an ongoing acquisition story. The immediate possibility is that Fynske Bank ups the bid with a revised share exchange ratio. After all, the regulatory hurdles have already been cleared. This would, however, require another premium to the current Nordfyns Bank share price of DKK468, which is a significant adjustment.

A second possibility, which could push the price higher, is that of an alternative bidder showing up at the door. So far, no one has. At the cancellation of the extraordinary general meeting, Nordfyns Bank announced plans to renegotiate with Fynske Bank, stating it was only speaking to Fynske Bank and that no other parties had shown interest. But this could change. The obvious candidate would be SJF Bank with its 25% ownership and a previous public statement by its CEO, Lars Petersson, of its intent to grow the bank by M&A (though not by responding to bidding invitations). Recently, SJF Bank issued bonds to bolster its capital, which it claimed was unrelated to the Nordfyns Bank situation. At SJF Bank’s latest AGM, a shareholder proposed this exact deal (a merger with Nordfyns Bank), but it was voted down.

Sydbank, which holds a 20% stake in Fynske Bank and considers it a “strategic” position, has a history of expanding on Fyn, having acquired Egnsbank Fyn back in 2002. Sydbank, of course, made a binding commitment to vote in favor of the merger on the Fynske Bank side. With that bid gone, Sydbank could itself step up.

Then you have the third-largest Danish bank, Jyske Bank, an avid acquirer that recently got back in the M&A arena after Danish competition authorities prohibited Nykredit, the 2nd-largest Danish bank, from withholding provision payments for mortgages written under its credit institution, Totalkredit, when the underwriting bank switches to a different partnering credit institution. Since Nordfyns Bank partners with Totalkredit and DLR Kredit, Jyske Bank would likely aim to transfer Nordfyns Bank’s mortgage business to its own credit institution, Jyske Realkredit.

Both Sydbank and Jyske Bank are on Bankdata as their banking core, lowering the hurdle to cost cutting.

So with a handful of potential suitors (including Ringkjøbing Landbobank, which has a history of regional expansion through its acquisition of Nordjyske Bank), the second question is what deal could land in Nordfyns Bank shareholders’ lap.

Nordfyns Bank

The origins of Nordfyns Bank date back to the 1890s when a group of local entrepreneurs founded Bogense Bank. After the Great Depression, the bank merged with Nordfyns Handels- og Landbobank and kept that name until 1985, when it was renamed Nordfyns Bank, reflecting a broader regional focus across Northern Fyn and an ambition to serve larger surrounding cities, such as Odense. By the early 2000s, Nordfyns Bank had seven branches, one fewer than today, and by the 2010s, it served ~30k customers, evenly split between private and commercial.

It does traditional banking, with privates taking up 43% of its credit exposure and SMEs 57% across a fairly diversified loan book (transportation, hotels, and restaurants are the biggest chunk, taking up 25%, but the bank has a nearly equally sizable large bond portfolio as well). It also runs a small, negligible (in terms of profits) commercial financing business through subsidiary Nordfyns Finans, spanning all of Denmark.

Nordfyns Bank is over-capitalized, sporting a 7.5x A/E and a 25.4% capital adequacy ratio, 14.2ppts above its individual solvency need. With loans-to-deposits at 42%, supporting a liquidity coverage ratio of 532%, the bank could run with more leverage to bump up returns on capital. Of its rather small loan exposure, 55% is callable, and of the 4.3% of total loans in arrears, about half are collateralized. A loan loss reserve of 4.8%, of which the discretionary reserve comprises 29%, is significantly above the average of its Group 3 bank peers.

However, instead of paying out excess capital, Nordfyns Bank has buffered up, paying out just 27% of earnings after hybrid interest to shareholders in FY24. And although this largely mirrors Danish banks in general, reflecting tightened capital requirements post-GFC,…

…a larger acquirer could release capital in a merger, especially if the acquirer bank is on an IRB model as opposed to the standard capital model (slightly mitigated by the introduction of an output floor to IBR models since January 1st this year). Smaller banks maintain higher solvency ratios because it takes resources to control solvency on a running basis just above capital requirements. Also, it’s more costly for smaller banks to raise capital quickly, so they hold extra capital for rainy days.

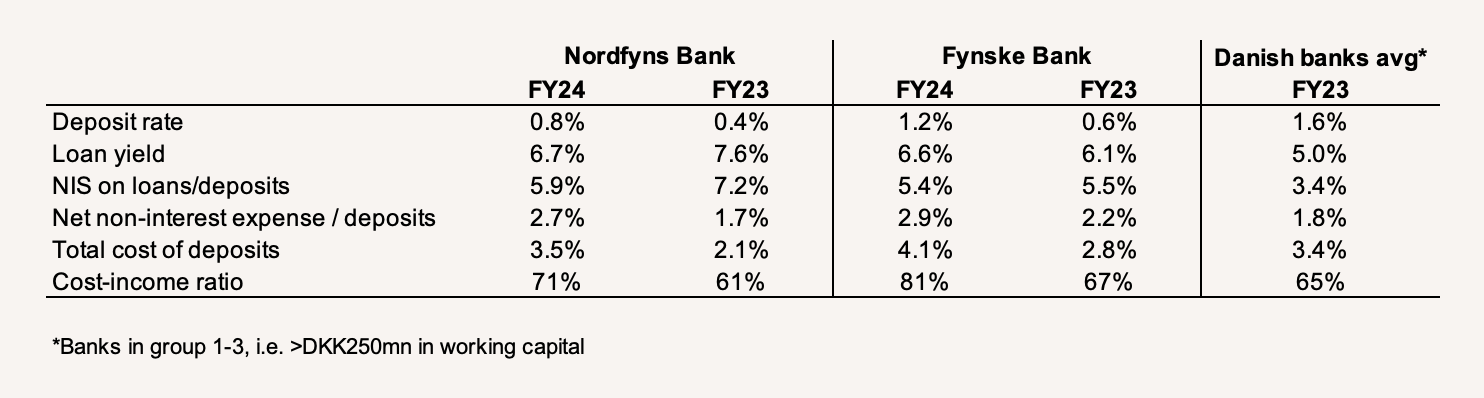

Nordfyns Bank’s earnings are liability sensitive. As inflation went haywire during 2022, causing the central bank (Nationalbanken) to hike its deposit rate faster than bank deposit rates, interest spreads widened. Danish banks, like Nordfyns Bank, didn’t increase loan rates at the same pace as they suddenly benefited from a long-missed income stream coming back on tap, earning interest at the central bank. Nordfyns Bank’s ROE jumped to 17% in FY23. Then, what followed a stop to central bank hikes was an increasing use of CDs and cash sorting with bank depositors, which narrowed net interest spreads. To make matters worse, this happened in conjunction with rising IT costs across the banking industry. I showed a cost-income ratio of 71% in FY24 above. In Q12025, this was 83%, which, together with a contracting spread, pulled core earnings down 51% year-on-year.

The worst may be over, but net interest income is likely to take a further hit in FY25. Competition is tough, particularly on loan rates for mortgage credit and electric vehicles, and customers still cash sort into higher-rate products. If we take management pre-tax earnings guidance of DKK55-85mn, with the top-end reflecting a 28% earnings drop from FY24 (though FY24 earnings quality was questionable, given one-third of pre-tax earnings came from value adjustments and loan write-ups), Nordfyns Bank trades on 12.3x net earnings, achieving a 9% post-tax ROE for FY25. Over the longer term, management aims for 6-9% ROE.

It’s hard to argue paying much more than 1x book for a bank like that. With a safe, over-capitalized balance sheet, you could argue that a risk-adjusted required return of something like 7-8% could justify a standalone P/B of 1x. But then you gotta add the takeout value, with synergies shared between the buyer and seller. If we take the Fynske Bank-Nordfyns Bank merger assumptions of DKK68mn annually, which is 34% of Nordfyns Bank’s cost base, then subtract taxes to get to DKK50mn after tax, then assume that those savings ramp up to full integration in year 3 (FY28), then DCF’ing that with DKK100mn after-tax one offs in year one and an 8% cost of equity, you could get to ~DKK500mn of synergy value. Assuming 50% of that accrues to Nordfyns Bank shareholders, added to a 1x book value, this is a justified value per share of DKK575/share, or 23% above the share price. An interesting risk/reward, as the downside is minimal at fair value, and you have a short-term catalyst from ongoing merger talks.

Is there potential for a pre-announcement risk arbitrage trade here? Sure. Nordfyns Bank is alluring, and I follow it closely, but there are other ways to play the Danish bank consolidation narrative. Many analysts have Danske Andelskassers Bank on the hotlist as a potential acquisition target, especially after Nykredit acquired Spar Nord, which previously tried to buy DAB and still holds a 32% stake. Other analysts have Arbejdernes Landsbank and Hvidbjerg Bank as potential targets too.

However, I’m eyeing another Danish bank that’s more attractive. This bank is way too cheap, with a setup equal to Nordfyns Bank before its 50% run up in one month. It’s less liquid (Nordfyns Bank trades ~DKK1mn/day), even for a microcap, but could be well worth the effort for smaller accounts. I’ll write it up in the next week or so. Stay tuned.