As urbanization continues its trajectory, especially in countries with rising middle classes, it’s evident that you, as an investor, would want to find a “toll road” company taking advantage of such a development. Elevator companies come to mind. An elevator installation predictably lasts for many years, often by the same age as the building in which it’s installed. And although elevator riders don’t pay a toll on every ride, the building owner does pay an indirect toll. The more an elevator is driven, the riskier it is to keep in operation, and the more maintenance, repair, and modernization are required, the more it leads to tremendous service fees to the vendor throughout the elevator’s lifetime.

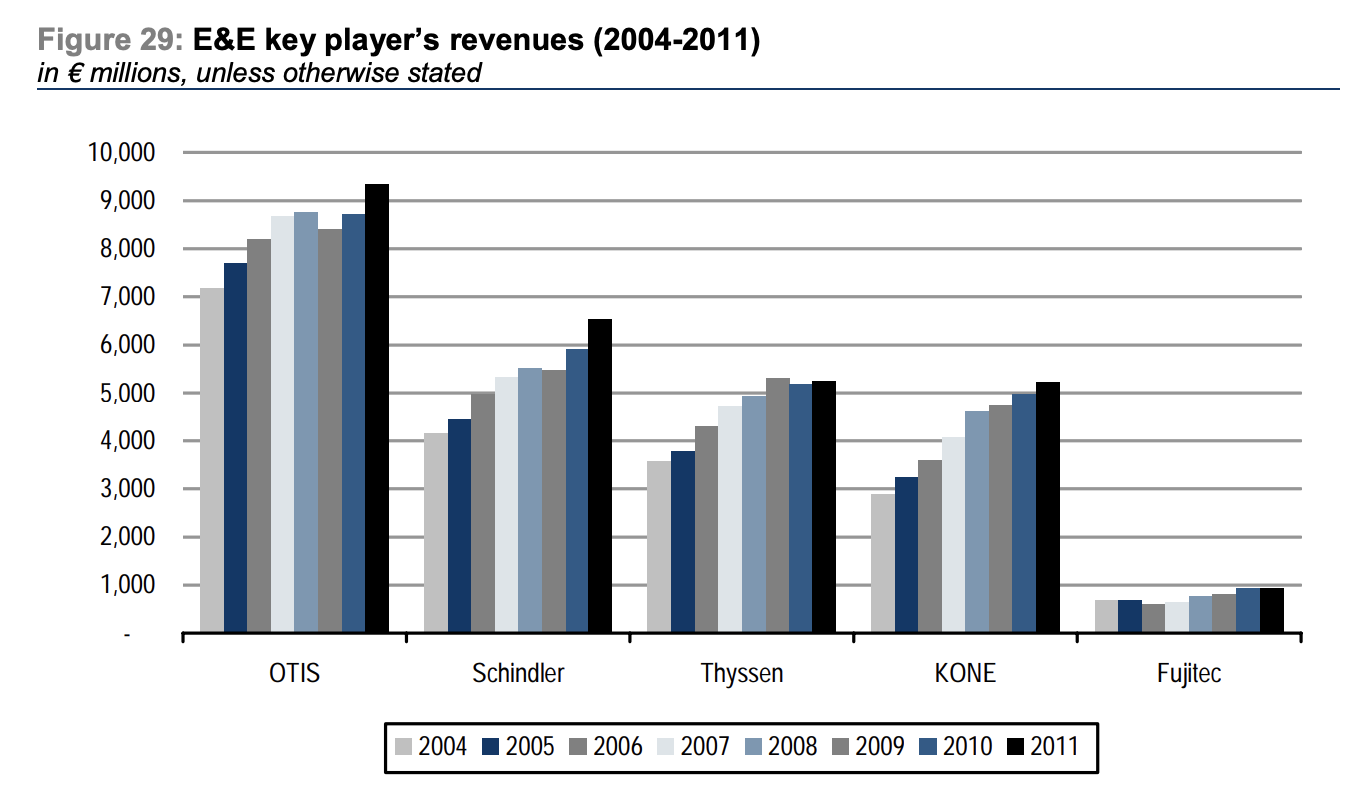

What’s to like about the elevator business is that it’s simple, predictable, and earns attractive returns on capital. Interestingly, the four major elevator players globally, Otis Worldwide, Kone, Schindler, and private equity-owned TK Elevator (in addition to several smaller players in APAC), are about the same size, give or take a few billion, trade around the same multiples, and share fairly similar economics. The world will always need elevators and escalators (it will need more as far as the eye can see), and given the security and trust involved with selecting a vendor, future business continuously accrues to one or each of the four major players, creating a natural oligopoly.

An elevator’s life begins at the construction of a building when one of the big four is hired to supply and install one or more elevators. Once an installation is done, the vendor turns it over to the owner and slaps on a 1-2- year service agreement that underlies the warranty of the elevator. Once that agreement expires, the owner is free to hire whoever they want to regularly maintain the elevator as mandated by law. What typically happens is that the owner, perhaps from inertia or risk aversion, decides to continue the service agreement with the vendor. After all, the vendor knows the product inside-out, is properly equipped to support the owner on any ad-hoc issues (at a price, of course), and has the spare parts to support it.

For the elevator vendor, it’s this latter stage, the service stage, that’s the good stuff — the bucket of gold waiting at the end of the rainbow. The installation itself is the riskier, more cyclical phase since it follows the cynical construction cycle, which in turn follows the debt cycle, is subject to labor and raw materials price swings in the construction process, and competitors bid aggressively to get their elevator inside the door. So, selling an elevator is in itself a mediocre high-teens gross margin business, but vendors are willing to jump through these hoops for the lucrative mid-30s to mid-40s gross margin service agreements (maintenance, repairs, and modernizations) that await once the job is done.

Because elevator maintenance is mandated by law, the work is dependable no matter the economic backdrop. And because these service agreements are sticky due to the reasons mentioned above, the durations, sporting >90% retention rates for the big fours, are long. An elevator is retired only once a building is pulled down or during an (infrequent) major conversion, so it can serve for up to 30 years. And since the service market isn’t just dependent on new elevator installs, but can also be managed by increasing conversion from new installations, improving retention, and recapturing off-portfolio units (those elevators that are installed by a vendor but are maintained by a third party), the result is that the service market continues to grow by msd% year after year. During 2006-09, stable growth in the service market was the primary reason why the elevator business remained broadly stable.

The customer who picks a service vendor is usually different from the one who initially makes the installation decision, so not every new installation ends up on the elevator vendor’s maintenance base. The general rule of thumb is that 2/3 of elevators installed convert to a service agreement once the initial service period wears out, but conversion rates vary significantly from 1) developed to developing countries and 2) by the scale of the project. For example, China, the world’s now biggest elevator market, accounting for 40% of the global installed base, has notoriously been a hard market for service conversion with an industry average of ~25% throughout the country’s construction boom. For comparison, conversions are >80% in Europe. Also, a major part of China’s construction boom has been in residential real estate, whereas the high >60% conversion is more often found in commercial real estate and skyscrapers. For smaller installations (eg, seven-story residential), rolling contracts usually run 1-2 years, whereas for larger installations (think hotels or airports), they may run 5-7 years years, implying a measly 1-2% annual attrition from an >90% retention rate.

Economics of density explains why new entrants face insurmountable barriers against the oligopoly. Servicing an elevator requires extensive training, and local mechanics have little incentive to become experts in an elevator that does not already have a large installed base, let alone carry an inventory of spare parts for it. Price matters little in this equation because safety is more important than the product for the customer, too. There’s also leverage in geographical density. ~70% of the cost structure of an elevator’s maintenance business consists of field costs, and of those field costs, ~40% can be split into unplanned callouts, indirect time spent, and travel time. A larger installed base equaling greater density and lower proximity between service work is an advantage that’s tough to compete with and which almost entirely explains Otis’s margin advantage of being the market leader with the significantly largest maintenance base: