A common thing about complex, dynamic topics such as economics, climate change, and politics is that people participating in such systems are often divided into two opposing camps with differing degrees of polarity: they’re either capitalists or socialists, believers or non-believers, right-leaners or left-leaners, etc. Portfolio management is another such topic. And two tugs of war have divided camps over many decades.

One involves the question of whether the stock market is efficient, where market prices fully reflect everyone’s rational expectations for the future. The other is about the question of diversification and how much you should diversify to optimize your risk-adjusted return. Here, the camps are not divided evenly. The vast majority of investors believe wide diversification to be the most important practice to minimize risk by minimizing portfolio volatility. It’s likely the most frequently given advice from financial advisers. Few believe low diversification—or concentrated investing—to be the less risky option. But is the camp where Buffett belongs.

In The Warren Buffett Portfolio, Robert Hagstrom illuminates how Buffett achieved his performance managing a concentrated portfolio with occasional huge bets. He calls it “focus investing”. This is Hagstrom’s second book on Warren Buffett. The first was The Warren Buffett Way. While the first book gave the reader tools to pick stocks wisely, this one shows how to organize them in a focused portfolio and provides the intellectual framework for managing them.

The book is divided into two parts: the first introduces focus investing and its main elements including academic and statistical rationales, and the second turns attention to other disciplines: mathematics, psychology, and the science of complexity. The book ends with Hagstrom giving guidance on how to employ a focused investment strategy.

Before people can successfully use the focus portfolio strategy taught by Buffett, they must remove from their thinking the constructs of modern portfolio theory. Ordinarily, it would be easy to reject a model that is largely considered intellectual; after all, there is nothing prideful or rewarding about being average.

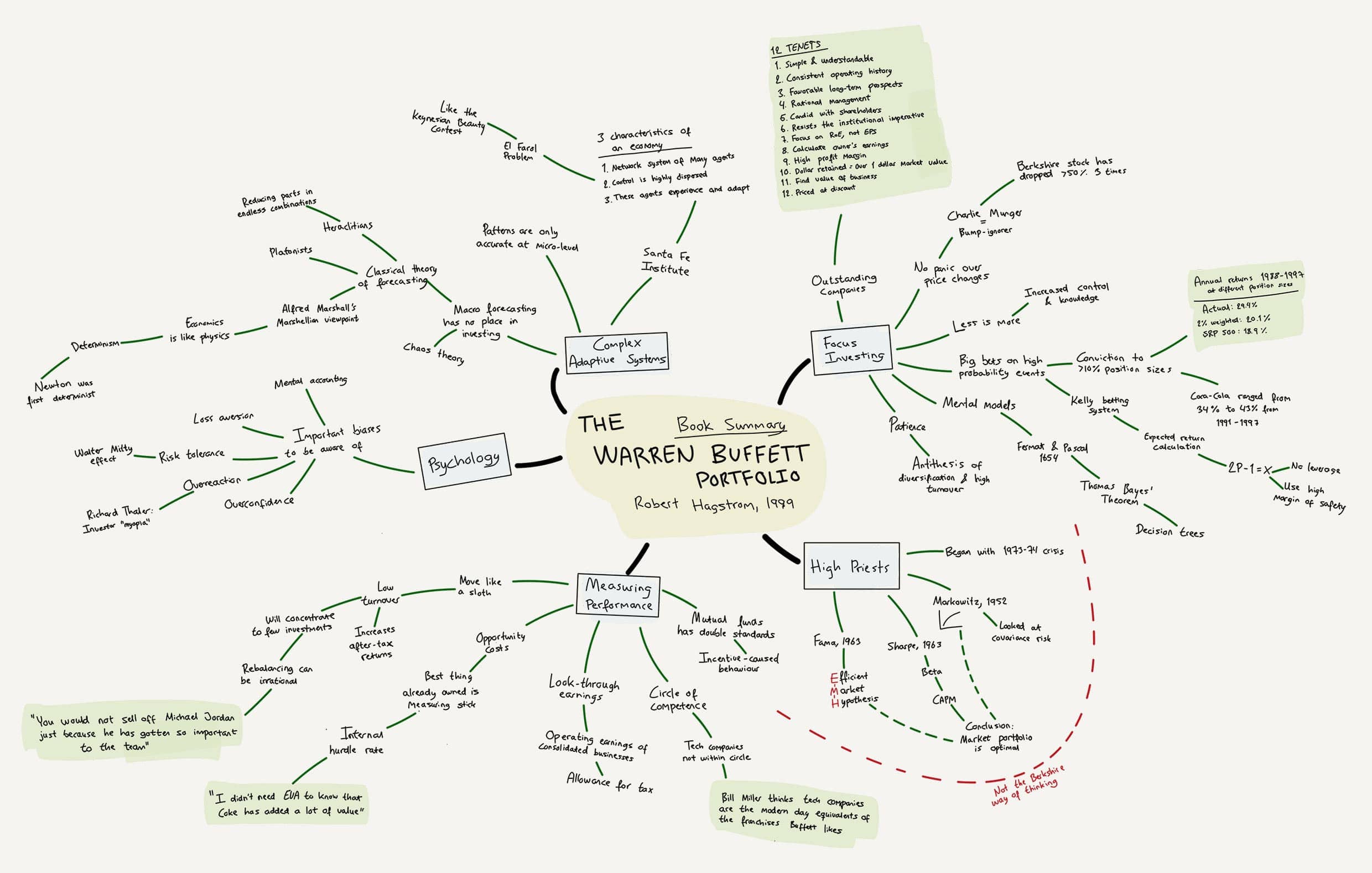

By listing the performance of other investors besides Buffett, including Phil Fisher, Charlie Munger, Bill Ruane, and Lou Simpson, Hagstrom underlines the argument for a focused portfolio by showing that the probability of beating the market goes up drastically when the size of the portfolio goes down. He then isolates Berkshire’s equity portfolio from 1988-97 where annualized returns were 29.4% compared to 18.9% from the S&P 500. This period includes Buffett’s jump into Coca-Cola which in 1988 represented 20.7%/Berkshire’s equity portfolio and later in the 10 year period represented up to 43%. Coca-Cola returned 34.7%/ year over the period.

Hagstrom then shows what would have happened if Buffett had not overweighted his positions but instead maintained an equal balance of his holdings through the period. On an equal-weighted basis, the portfolio would have delivered 27%/ year. He then shows that if Buffett had run a widely diversified portfolio of fifty market-returning stocks, he’d have generated a 20.1%/ year return—1.2 percent better than the market, excluding trading costs. He uses the Kelly criterion to explain Buffett’s big bets on what he perceives as high-probability events.

Even John Maynard Keynes was a focus investor. Proof of his investing record is in the performance records of the Chest Fund at King’s College in Cambridge from 1928 to 1945. Keynes outlined the fund’s investment policy report to only include concentrated investments in a select few common stocks of high-quality predictable businesses using fundamental analysis to estimate a price below value. During his 18 years running it, although there were periods of higher-than-market volatility and underperformance, he in the end returned 13.2%/ year while the UK stock market remained flat. As Hagstrom writes: “Considering that the time period included both the Great Depression and World War II, we would have to say that Keynes’s performance was extraordinary.”

“It’s a mistake to think that one limits one’s risks by spreading too much much between enterprises about which one knows little and has no reason for special confidence… One’s knowledge and experience are definitely limited and there are seldom more than two or three enterprises at any given time in which I personally feel myself entitled to put full confidence.”—John Maynard Keynes

Another aspect of focus investing strategy is what Hagstrom calls “moving like a sloth”: an aversion to activity and low portfolio turnover.

As long as things don’t worsen, the idea is to let your investment run for at least 5 years, through the bumps of volatility with equanimity and your perception of intrinsic value intact. Excessive trading in an attempt to anticipate market moves is not the Buffett way. And due to capital gains tax on realization, the long-term investor has an advantage in achieving higher after-commission and after-tax returns over many years with a low turnover portfolio. Buffett’s baseball analogy is highlighted once again. Investing is a series of pitches, and to achieve above-average performance, you must wait until an opportunity arrives in the “strike” zone. Buffett believes investors swing too much at bad pitches, and that it’s perhaps not that investors are unable to recognize a good business at an attractive price when they see one, but the fact that they can’t resist swinging the bat.

“You only have to do a very few things right in your life so long as you don’t do too many things wrong.”—Warren Buffett

A human tendency is the desire for order, balance, unity, and symmetry. In portfolio management, this tendency is reflected in regression to the mean: the expectation that high-rising assets eventually must fall and poor performers must again rise. The expectation of regression to the mean is why portfolio management strategies usually involve rebalancing. When a holding becomes disproportionally large in a portfolio, the manager trims the position to “lock in gains” and bring it down to a pre-determined target weight. But while regression to the mean is a common statistical phenomenon, it can be equally dangerous to assume it exists in every system. What often happens in the stock market is that industry economics and sustainable competitive advantages result in certain types of companies continuing to over-perform and poor companies continuing to drift. Buffett doesn’t believe in rebalancing. In a portfolio built for capital appreciation with a long time horizon, rebalancing makes little sense and can be a headwind to the Kelly criterion.

As Buffett describes it:

“You would not sell off Michael Jordan just because he has gotten so important to the team.”

The conventional way risk is being taught in finance is by price volatility as a direct proxy for the risk of the company. This has allowed academics to quantify and isolate the risk component of an investment into a direct input in valuations and statistical models. Buffett has a different definition of risk. He defines risk as whether after-tax returns from an investment “will give [the investor] at least as much purchasing power as he had to begin with, plus a modest rate of interest on that initial stake.” Buffett’s primary concern is “business risk”, not market risk. He thinks of business risk in terms of what can happen over many years that could destroy, modify, or reduce the company’s economic strength. It’s not quantifiable like beta. Investors tend to let the irrational behavior of the stock market cause them to behave irrationally as well. Increased short-term volatility can be a gift to the focus investor.

“If the investor, instead, fears price volatility, erroneously viewing it as a measure of risk, he may, ironically, end up doing some very risky things.”—Warren Buffett

Buffett believes it makes no sense to try to forecast political and macro-economic trends and that such projections are an expensive distraction in investing. Hagstrom walks the reader through classical theories on forecasting such as the Marshellian viewpoint and Newton’s determinism, which was when economics started to be treated as physics, using (false) precision. He then introduces the Santa Fe Institute which specializes in multi-disciplinary studies of complex adaptive systems. Michael Mauboussin, who sits on the board of trustees (now Chair), describes a story called the El Farol problem which uses a bar attendance analogy for the type of game theory problem that exists with trying to predict the market. Just as with the Keynesian Beauty Contest, the experiment describes the characteristics of a complex adaptive system where the actual result is determined by the forecasts of others. There’s a difference between understanding a complex adaptive system and how to predict it.

“We have two kinds of forecasters, those who don’t know and those who don’t know they don’t know.”—John Kenneth Galbraith